3 - Realities of Sustainability: Profit

Lesson 3 Overview

Lesson 3 Overview

Summary

My intent in covering the Profit pillar of sustainability third is very specific:

In Lesson 1, we begin in Planet, the first and only sustainability aspect most people tend to think about (and therefore think that they know), and show the tremendous breadth in how organizations define and measure.

In Lesson 2, my intent is to move you a little more into the 'deep end' of Sustainability, into the even more esoteric and complex People aspects. This is where hopefully you are able to see how much research and understanding is needed to understand the actual content of a CSR before we can evaluate it. For example, how could we possibly speak intelligently about how two organizations compare on "Worker Satisfaction" if we are solely reliant on their own metrics and data, and one obfuscates and the other misattributes?

In this Lesson, my intent is to snap you back into the aspect of Sustainability the public always takes for granted, but yet, is what allows an organization to take on its noble purpose at all. Even in the case of a pure charity, if operating expenses outstrip the ability to fundraise or otherwise generate funding, insolvency awaits.

For me, personally, Profit is the most exciting pillar in many ways, as it is what allows an organization to expand on their VMVs. Perhaps more than simply a 'nice to have' or a 'mission stimulant,' it is the oxygen of the organization.

The other aspect I hope to develop in this Lesson is that many 'nuts and bolts' organizations have done wonderful things in terms of waste reduction, product development, lifecycle, and efficiency under the auspices of "profitability." These organizations do the yeoman work of sustainability without sometimes even realizing it.

Learning Outcomes

By the end of this lesson, you should be able to:

- discern the material aspects for a sustainability program and their importance;

- evaluate an organization's approach to Profit issues through the lens of their stated Vision, Mission, and Values;

- argue the relationships between sustainability, profitability, and long-term strategy of an organization;

- differentiate sustainability-centric product offerings and strategies (revenue positive) from sustainability programs;

- articulate the role of risk mitigation and regulatory compliance in sustainability.

Lesson Roadmap

| To Read | Chapters 5 and 6 (Keeley, et al.) Documents and assets as noted/linked in the Lesson (optional) |

|---|---|

| To Do | Case Assignment: IKEA

|

Questions?

If you have any questions, please send them to my axj153@psu.edu [1] Faculty email. I will check daily to respond. If your question is one that is relevant to the entire class, I may respond to the entire class rather than individually.

Materiality and Sustainability Imperatives

Materiality and Sustainability Imperatives

What Was Once Intangible Now Becomes Immediate

In discussing sustainability with colleagues–or frankly anyone, after discovering you work in the field of sustainability–you may find two questions tend to be asked in one form or another:

- "Where is all of this sustainability stuff coming from?"

- "What does it mean to our organization?"

In both cases, materiality is a significant part of the answer, and there are two definitions of materiality which are equally important in stating our case: the formal Supreme Court definition of materiality in reference to financial reporting, and the functional definition of materiality as applied to each organization. Both are extremely important for shaping sustainability within the organization, and these two cores of materiality tend to be invaluable in explaining sustainability to anyone from a classroom of 10-year-olds to your organization's leadership (which may have strikingly similar attention spans!).

What is fascinating about the two cores of materiality is that they tend to capture much of the essence of sustainability as practiced in organizations today, as the Supreme Court definition captures the external requirement, and the functional definition tends to capture internal imperatives and what makes the sustainability program unique to the organization. For this reason, materiality is also what makes the practice of sustainability so varied from one organization to another, as there is no standard "sustainability playbook" an organization can dust off and execute. For example, an excellent sustainability program for Nike would, at best, be a poor fit for Ford.

The Formal Supreme Court Definition of Materiality

{kind=link}

In 1976, the U.S. Supreme Court rendered a judgment in TSC Industries, Inc. v. Northway, Inc [5], creating a more defined definition of what information should indeed be considered material in financial disclosures, especially for publicly traded companies.

In summary, the case dealt with a merger between National Industries and TSC Industries where there had been some intermingling of board members and a significant share of company stock had traded hands before a merger vote, but this interaction was not disclosed to shareholders. In the case, Northway, a TSC shareholder, argued that the various pre-merger intermingling of TSC and National could have been construed as a conflict of interest, and would have caused them to therefore vote against the merger.

The earlier definition of materiality, as interpreted by the Court of Appeals in this case and recalled in the Supreme Court judgment was that, "...material facts include all facts which a reasonable shareholder might consider important." The Supreme Court believed that this Court of Appeals interpretation of material information was far too broad, and in a unanimous decision, Justice Thurgood Marshall penned an extremely important line in the Case Opinion:

...there must be a substantial likelihood that the disclosure of the omitted fact would have been viewed by the reasonable investor as having significantly altered the "total mix" of information made available.

This simple line would, in time, be the sentence that launched a thousand sustainability programs. This line is why sustainability programs are no longer "optional" for publicly traded companies, and why those publicly traded companies, in turn, "push down" sustainability requirements and audits into their suppliers. What those third-party suppliers do–for example, manufacturing shoes with child or indentured labor–is indeed a risk and material concern for the company purchasing from that supplier.

Let's all put on our black hats and question this in practice.

With our blackest-black CFO hats now firmly secured atop our collective consciousness, let's assert that nothing a company does with 'carbon emissions' or 'recycling soda cans' is going to change either the top or bottom line of the company, and that only "activist" investors would ever care about sustainability in determining whether to invest in a company or not.

What is the likelihood that not disclosing information such as the following would 'significantly alter the total mix of information made available to a reasonable investor'?

- that 20% of a company's branded apparel (accounting for 40% of revenue) is made in factories utilizing child labor

- that a highly-respected premium consumer brand is a human rights violator

- that a company has nearly 10x the reportable injuries of peers

- that a company suppressed whistleblowers from reporting a potentially-fatal product flaw

- that a company's product portfolio energy performance lags peers by 50%, with no plans to improve

- that a company relying heavily on green badging and "sustainable sourcing" has absolutely no proof of claims

If these types of issues indeed affect the "total mix" of information made available and have bearing on share value, then sustainability aspects are indeed material to the organization... and are, therefore, legally required public disclosures.

The Sustainable Accounting Standards Board (commonly referred to as SASB in text, pronounced 'sass-bee'), a 501(c)3 created to help create uniform standards for materiality disclosures (and chaired by Michael Bloomberg), further illustrates the point, bridging the Supreme Court finding with existing required disclosures for public companies (SASB, 2015) [6]:

Disclosure of material sustainability issues is important to investors, companies, regulators and the public for the following reasons:

- The SEC already requires disclosure of material issues in the Form 10-K, 20-F and other filings in use by investors.

- Institutional investors have a fiduciary duty that requires them to consider material issues.

- Companies have limited resources, and must therefore focus on disclosing and managing the performance of material issues.

- The potential for negative social and environmental impacts of operations can present high costs to investors, companies and society.

The Functional Definition of Materiality

GRI offers a short explanation of materiality principle as applied to an organization's sustainability program, stating it as aspects that "Reflect the organization’s significant economic, environmental and social impacts; or Substantively influence the assessments and decisions of stakeholders" (GRI, 2013) [7]. While this is certainly accurate, I tend to favor the more picturable definition of the GRI Materiality Tests [7]:

In defining material Aspects, the organization takes into account the following factors:

- Reasonably estimable sustainability impacts, risks, or opportunities (such as global warming, HIV-AIDS, poverty) identified through sound investigation by people with recognized expertise, or by expert bodies with recognized credentials in the field

- Main sustainability interests and topics, and Indicators raised by stakeholders (such as vulnerable groups within local communities, civil society)

- The main topics and future challenges for the sector reported by peers and competitors

- Relevant laws, regulations, international agreements, or voluntary agreements with strategic significance to the organization and its stakeholders

- Key organizational values, policies, strategies, operational management systems, goals, and targets

- The interests and expectations of stakeholders specifically invested in the success of the organization (such as employees, shareholders, and suppliers)

- Significant risks to the organization

- Critical factors for enabling organizational success

- The core competencies of the organization and the manner in which they may or could contribute to sustainable development

Capturing Materiality: The Materiality Matrix

To set the boundaries of what aspects and considerations an organization considers specifically material to their operation, they create a materiality matrix. What is interesting about this chart or table is that it bridges the two cores of materiality in a rather illustrative and easy to understand format. We will do a bit of comparative analysis in a moment, but I'd like to briefly cover the process underlying the creation of a materiality matrix.

The organization begins by creating a full list of issues and aspects it faces, doing so both by internal meetings and external stakeholder engagement. These issues could range from minor concerns raised by an NGO to aspects which could potentially trigger the Supreme Court definition of materiality insofar as the omission of the information could alter "the total mix of information made available." Each aspect's materiality is then rated according to two standards, arranged on the X and Y axis:

In the X axis, usually referred to as "Organizational relevance" or "Organizational impact," the organization rates the importance of a given issue to its operations and viability. The act of creating this evaluation tends to be voted and argued by a broad team representing the various functions of the organization from marketing to EHS. Some companies are extremely scientific in this regard, creating weightings for the various functions based on their knowledge of each specific issue at hand, while other organizations essentially throw the issues up on the wall and vote to create a rank order.

In the Y axis, usually referred to as "Stakeholder concern" or "Stakeholder relevance," the organization then engages external stakeholder groups to understand how they would rate the importance of a given aspect.

Interestingly, there are issues which organizations consider a significant risk given their knowledge of operations, but which stakeholders may have no idea of, and vice versa. This is what makes materiality matrices so powerful, as they represent the entire field of issues and aspects to be considered, in turn guiding them toward the most important for both the organization and stakeholders.

Similarities and Differences in Materiality: An Example in Chocolate

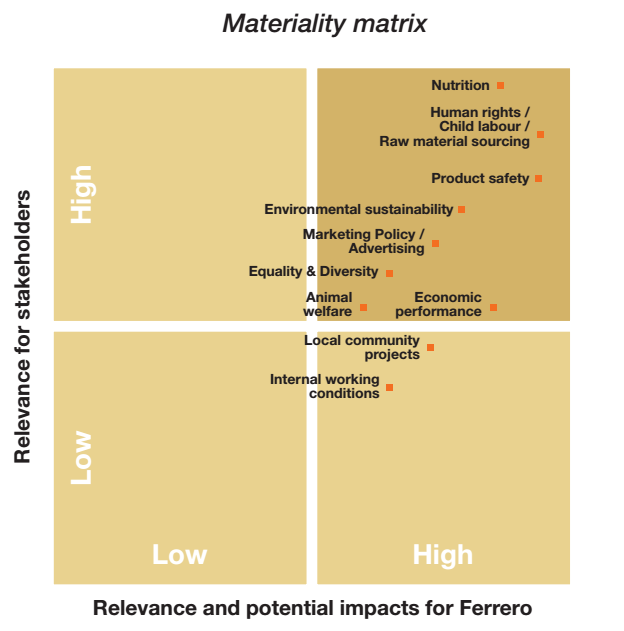

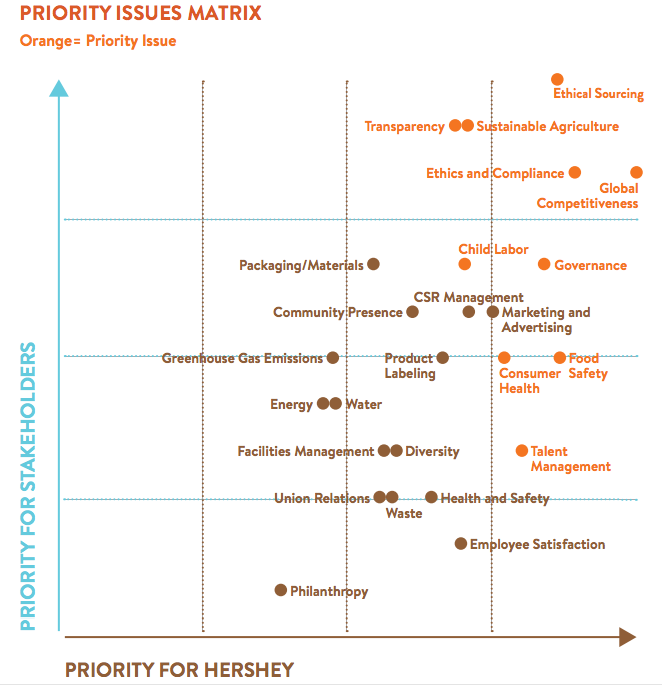

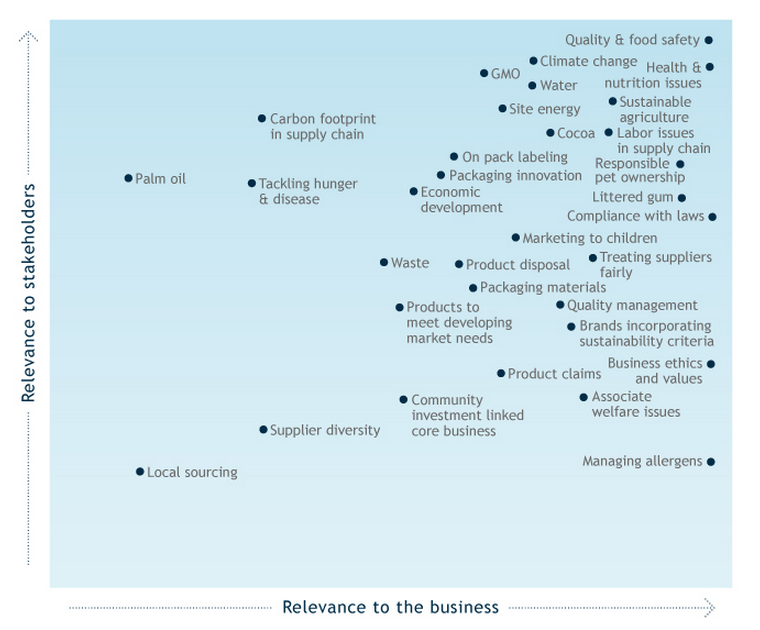

To illustrate how varied material issues can be in similar organizations, let's examine the materiality matrices of four of the world's leading chocolate companies: Mars, Nestle, Hershey, and Ferrero. As we will explore in later lessons, comparative analysis of materiality matrices is an excellent way to unearth shared issues and opportunities for innovation, as well as revealing aspects an organization may be ignoring that its peers are addressing.

Check Your Understanding

Look through the four materiality matrices below and consider underlying similarities and differences.

- Is there untapped potential or shared need which could be used as a platform for innovation?

- Are there issues being ignored based on your understanding of the industry?

- Any interesting disconnects or ratings which would merit further exploration?

- Are there potential entry points to displace existing suppliers or reinforce existing relationships?

If you would like, jot a few notes below... and then click the link to reveal sample areas of interest.

Click for areas of potential interest.

- Health/Nutrition is a top 2 concern for all companies, except Hershey's, where it is ranked below aspects like "Governance" and "CSR Management" for stakeholders, which is odd given the heavy public emphasis on obesity, food deserts [8], and other nutritional concerns. Furthermore, Hershey itself shows it as their #6 issue. This is interesting and bears research.

- All have some flavor of food/product safety in mid-pack, but Ferrero rates it as #2 overall. This may be a very fitting approach given their past experiences with their popular Kinder Eggs (chocolate eggs with toys inside) being banned in the US [9] as a choking hazard for nearly 40 years. Notably, Ferrero takes a head-on approach to this issue, devoting 10 pages in its CSR specifically to Kinder Egg toys (beginning p.17 in linked PDF, p.30 on printed page). [10]

- "Littered gum" is unique to Mars, and may be an interesting read. Another example of how tailored materiality is to each organization, even within subsets of industries (Mars owns Wrigley Gum).

- "Community presence/economic development" was a bit lower than one might expect, given that much of the supply chain is in impoverished areas. This may be either a function of robust programs in place, or simply of a lower relative priority. Bears investigation.

- There are a few "entrance points" for suppliers... "Packaging innovation" and "Packaging/Materials" both ranked fairly high priority for Mars and Hershey's, respectively. I would be interested, of course, if I were an industrial designer, packaging company, or existing supplier to either of those companies. Furthermore, these are likely bellwethers that those companies are also concerned with waste minimization in their own manufacturing operations... again, an opportunity. If I supplied disposable goods to those manufacturing operations, I would proactively reach out to see what we could do to understand/partner/improve performance.

- 'Responsible marketing' is a fairly high priority all around, which would be interesting to anyone from an ad agency with specific expertise to a consumer behavior research firm proposing a study to understand what responsible marketing is.

If we wanted to deep dive, we could begin by breaking out equivalent issues in a pivot table or spreadsheet and looking at average ranks, etc. to find further "threads to pull."

Ferrero Materiality Matrix - Click on image for larger version [11] [11] |

Hershey Materiality Matrix - Click on image for larger version [12] [12] |

Mars Materiality Matrix - Click on image for larger version [13] [13] |

Nestle Materiality Matrix - Click on image for larger version [14] [14] |

As covered in the "areas of potential interest" link in the exercise above, when a company lists its organization-wide strategic and tactical needs in a tidily prioritized form, it acts as a beautiful opportunity to innovate, find entry points, identify needs, and even to deepen relationships.

Here's the metaphor I would like to use: Imagine if you were a contractor, and you could freely walk into every house in town, and every owner had clearly marked their construction needs (i.e., "energy savings," "new paint," "child safety improvements") along with how important each project was to their family. Not every project would fit your expertise or strategy, but you could imagine that maybe... perhaps... it might be possible to find some opportunity there.

Needless to say, we will be exploring how to leverage materiality in innovation and creating offerings in later Lessons.

An emerging tool for both setting and evaluating an organization's material aspects is the SASB Materiality Map [15], which seeks to standardize material aspects by industry and sub-industry, as well as weighting relative importance. It's an interesting tool, and you can take a look at an early version in the linked page (red "Launch Map" link lower on page).

While organizations will always have unique issues to address (for example Ferrero's emphasis on product safety due to Kinder Egg line), the adoption of materiality standards could at least help create uniformity for the core aspects to make comparisons and benchmarking a bit more straightforward.

Profitability and Added Value

Profitability and Added Value

As we will be devoting the majority of this course to understanding how we can innovate and leverage opportunities in sustainability, I would like to take this section to provide two readings examining correlations between high performing sustainability programs, increased organizational profitability over peers, and leading management processes.

Optional Reading:

The Business of Sustainability: Imperatives, Advantages and Actions [16]

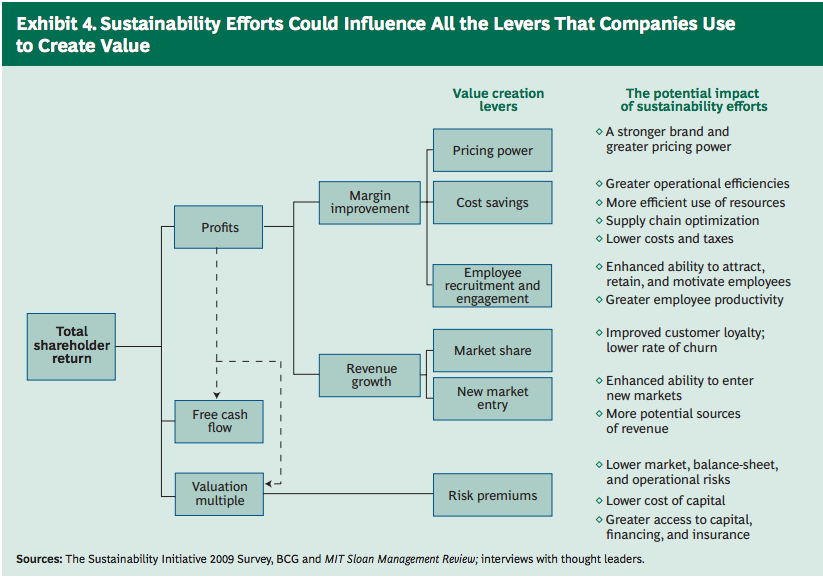

The first reading is jointly authored by The Boston Consulting Group and MIT Sloan Management Review, and reflects survey results from more than 1500 executives and high-level managers, and in-depth interviews with more than 50 thought leaders. It has quite a few interesting insights into sustainability's benefits to the business model and profitability, but below is one which nicely illustrates the ties between shareholder return and sustainability efforts.

Click to view a text version

The potential impact of sustainability efforts includes:

- A stronger brand and greater pricing power

- Greater operational efficiencies

- More efficient use of resources

- Supply chain optimization

- Lower costs and taxes

- Enhanced ability to attract, retain, and motivate employees

- Greater employee productivity

- Improved customer loyalty; lower rate of churn

- Enhanced ability to enter new markets

- More potential sources of revenue

- Lower market, balance-sheet, and operational risks

- Lower cost of capital

- Greater access to capital, financing, and insurance

Optional Reading:

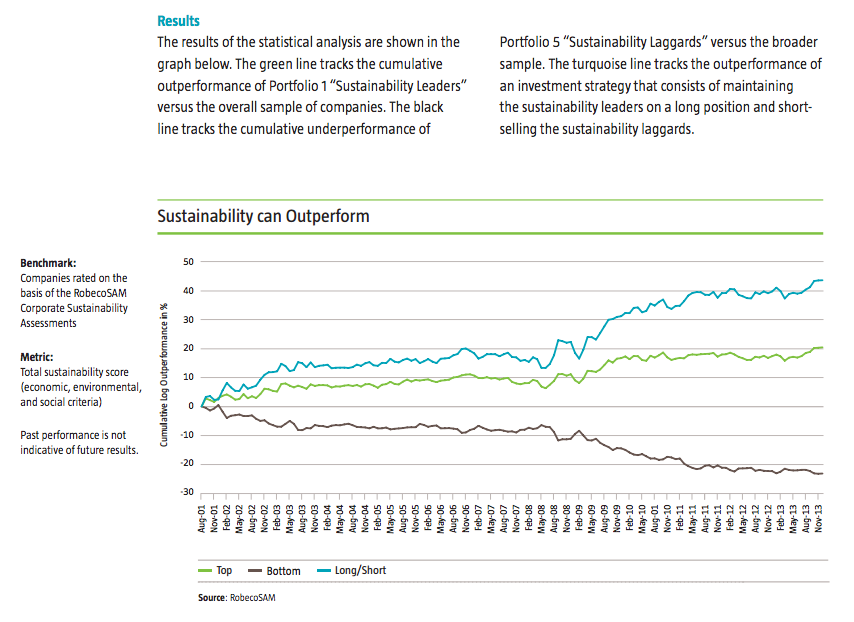

This is a shorter piece, centered on one, rather in-depth analysis of long-term performance. RobecoSAM, the auditing firm known for its international Sustainability Yearbook [19] rankings, examined the sustainability profile of more than 500 companies a year over a 13-year dataset to create a five-level tier of their approach to sustainability. From Leader to Laggard, they then evaluated the financial performance of those companies over the same period. Below is a central finding of that research:

Click to view a text description

Compartmentalized v. Infused Sustainability

Compartmentalized v. Infused Sustainability

Financial Benefits are Known, But Difficult to Unlock

To the public at large, the concept of sustainability tends to be associated with the color green, but those in the sustainability profession know far better that our work on a daily basis is dominated by the color gray.

Sustainability is one of those ventures which requires broad-based cooperation within an organization to have a chance of succeeding, but it can be difficult to know what that looks like. Metrics and surveys can reflect far more positive outcomes than are actually happening within the organization, and can signal far more progress than is actually taking place. Why? Because time and time again, experience and research tells us people are notoriously bad at self-reporting and predicting behavior, even when acting with the best of intentions. In fact, self-reporting is so poor in its performance of actual behavior that there are a few consumer research methodologies designed to use shifts in self-reporting after a distraction exercise –not the actual self-reported scores themselves–to measure sentiment. More on that later.

In talking to practitioners, it tends to be stories and episodic experiences more than survey results that signal the program is moving in the right direction:

"The product development team brought us into the early-stage design criteria last week."

"Legal has started to give sustainability a seat at the table in identifying risks to the organization."

"We've really started getting support from the business units on lifecycle analysis."

What is especially unique about sustainability's shade of gray is that even though it tends to have formal support at the C-suite level, sustainability programs tend to face a unique set of goals and constraints:

- Dedicated headcount tends to be very low. In 2013, a year that Caterpillar made $55.7B and had somewhere around 118,000 employees [23], it had three–three [24]–dedicated sustainability employees.

- Because dedicated headcount is low, sustainability programs tend to use employees and resources that "report to someone else."

- Sustainability budget for initiatives is many times formed at the individual project level, and therefore fluid.

- Success can be heavily dependent on how many business units are willing to proactively share.

- It ties to virtually every function within a business, so it does not have a single fixed role.

- It may be perceived in some organizations as a hindrance more than a help (for example, the work required for ISO 14001).

- Without conscious work and lobbying, it probably does not have revenue or sales applied to its work.

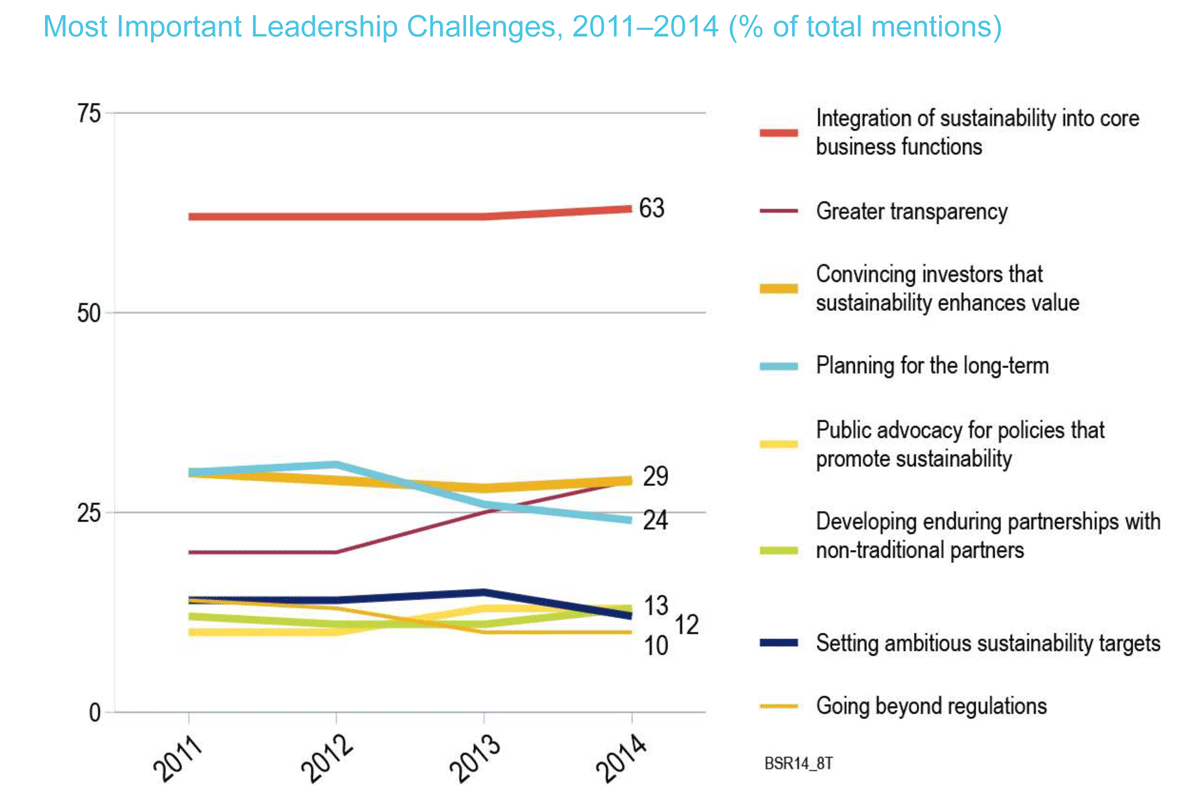

In its State of Sustainable Business Survey 2014 [25], BSR and GlobeScan surveyed more than 700 experienced sustainability professionals about a range of topics, but the question relating to sustainability leadership challenges underscores the point at hand:

Of all the potential challenges facing a working sustainability program, it isn't a challenge of resources, it is a challenge of integration of sustainability into the core of the business. But the question then becomes, if we know all of the acknowledged benefits of a robust sustainability initiative to the organization, how then can it be a question of integration? It would seem that the answer to that question is sometimes related to sustainability's broad reach, making it difficult to integrate deeply into only a handful of functions... there is so much to be done that the programs end up taking very finite people resources and try to do too much.

In going beyond rote integration and looking at motivations, actions, and organizational frames for sustainability, we may also consider that there is no one type of integration. In fact, one of the types of organizational integration of sustainability actively works to erode the reach of the program.

Compartmentalized Sustainability

Chances are many new sustainability programs, even with significant support from management, will function in a compartmentalized way for a significant period of time. Despite best efforts, many sustainability efforts may never leave a place of compartmentalization. What is meant by compartmentalized sustainability is, literally, sustainability is a discrete function within the organization, and that function is overwhelmingly isolated to a special set of specific initiatives.

For example, if a large customer of the organization has their own sustainability program and supplier reporting requirements and sends an 80 page questionnaire to be completed, chances are it will land on the desk of the person with "sustainability" in their title to decipher and complete. Speaking with colleagues at publicly traded companies, and especially those supplying raw materials or components, completing these surveys is a 20-hour a week effort for someone on their staff to complete the basic surveys and requires more time and information gathering to answer first-time questions.

Needless to say, completing these surveys can be a significant time drain, and can have a consequence of preventing the sustainability folks in an organization from taking on their own proactive projects. So, the program has a difficult time gaining the necessary reach within the organization to affect change or institute proactive work.

Infused Sustainability

To achieve the types of financial and organizational benefits described earlier in the readings in this Lesson, sustainability is not a role, it is a core function of the organization, and lives everywhere. In these types of organizations, the number of people with "sustainability" in their title may be the same as organizations with compartmentalized sustainability, but the role of sustainability becomes one which is far more about enabling others internally.

When sustainability is infused, it may have been originally shepherded in by a passionate founder or CEO, but it tends to be perpetuated by a genuine value for being a sustainable organization and one which succeeds and leads. So while the intent and basic knowledge of sustainability may be throughout the organization, there is typically the need for resources to provide more insight, find resources, and tie it all together. This is the role of the sustainability team: to assist the rest of the organization in their infused sustainability efforts and act as keepers of central information and strategy.

Naturally, the next question is something like, "OK. So how does one infuse sustainability into the organization?" Well, there's certainly no single or easy answer to that question. Otherwise, that 63 % of organizations having trouble integrating sustainability into the organization would have likely found the solution long ago.

I will say this: Many of the methods and philosophies we will employ in creating sustainability-driven innovations in this course can just as easily be applied within an organization as to create an offering. Furthermore, showing–not telling–what sustainability can bring to the organization through the creation of new offerings can go a long way to get people in an organization interested in what they can do, as well. We have seen this first-hand.

So, in understanding how this all ties back to Profit as a 3P imperative in the organization, it is important to consider that infused sustainability reinforces the profitability and prosperity of the organization just as much as the profitability of sustainability-related offerings can work to create infused sustainability within the organization. It really is a cycle of prosperity... or at least a "chicken or egg" arrangement.

Operational Efficiency

Operational Efficiency

Lean: Sustainability's Blue-Collar Brother

In understanding operational efficiency for many of the world's corporations, two systems of thought tend to predominate: the Toyota Production System (TPS, more broadly known as "Lean") and Six Sigma.

Although Lean and Six Sigma are systems used to create, hone, and, over time, optimize virtually any process or system, it is important to note that a central concern of each is the elimination of waste. While sustainability may deal with the longer-term ramifications of overuse and waste, as well as other wide-ranging implications, this expression of sustainability on the plant floor is as elegant and brutally efficient in intent as it is in execution: Waste costs measurable amounts of money. Period. There is no nuanced interpretation, no delicate interpretive dance of language to be had here, which is perhaps why the application of these systems are so popular with CFOs and operations management alike.

Underscoring some of their shared underpinnings, Lean and Six Sigma share essentially the same definitions of waste:

- Inventory is the excess products and materials not being processed.

- Talent is understanding people's talents, skills, and knowledge.

- Waiting is the time wasted waiting for the next step in a process.

- Motion describes the unnecessary movements by people (e.g., walking).

- Defects are the efforts caused by rework, scrap and incorrect information.

- Transportation is the unnecessary movements of products and materials.

- Overprocessing makes more work or higher quality than is required by the customer.

- Overproduction is production that is more than needed or before it is needed.

In consideration of what is a shared prescription of two of the dominant efficiency systems in the world, let's consider the sustainable underpinnings of the eight wastes and the types of aspects related to each waste:

| Lean Waste | Examples of Related Sustainability Aspects |

|---|---|

| Inventory Waste |

|

| Talent Waste |

|

| Waiting Waste |

|

| Motion Waste |

|

| Defects Waste |

|

| Transportation Waste |

|

| Overprocessing Waste |

|

| Overproduction Waste |

|

Especially in regard to sustainability's efficiency imperatives, we may find that the Lean/Six Sigma waste principles as practiced today are far more advanced and prescriptive than any GRI report or sustainability management system when it comes to the overall consideration of all types of waste. Where GRI may be far more focused on the defined wastes and setting indicators, Lean/Six Sigma takes a more holistic view in opening the facility to see the less obvious, but equally erosive, wastes.

Furthermore, and of key interest for our efforts in creating sustainability-driven innovation, is that the last 30 years of heavy worldwide adoption of these management systems presents us with ample numbers of cognitive "hooks and anchors" from which we may build a platform. For anything from beginning a sustainability initiative internally to creating a B2B offering, the philosophies of sustainability may already be deeply embedded in the organization already: they call them Lean/Six Sigma.

As we will cover in coming Lessons, our goal then is not to unnecessarily create new ideas (which is difficult, and frankly, expensive), but to build on and extend the thoughts, feelings, and frames that already exist in the in the minds of customers.

Caterpillar's Use of Six Sigma in Supply Chain Sustainability

Caterpillar is arguably one of the foremost adherents to this efficiency thinking, applying Six Sigma at very high levels throughout not only its organization, but the organizations within its supply chain. In a sense, this push functioned as a very proactive effort on the part of Caterpillar to drive efficiency and waste reduction in its suppliers and to allow its suppliers to work together to find ways to become more efficient. A few highlights from a Gillett, Fink, and Bevington piece in Strategic Finance [30] about Caterpillar's use of Six Sigma:

In addition to its own use of 6 Sigma, the company has taught its suppliers and dealers about the benefits of using the technique to refine the entire sales model. Caterpillar has introduced 850 suppliers worldwide to 6 Sigma, which has created more than 1,000 supplier Black Belts to help run the projects. One supplier that said it was interested in the Caterpillar 6 Sigma methodology allowed Cat to consult and transform the business. When implementing 6 Sigma, Caterpillar used facts and data to show the results the supplier could expect, so it didn’t take long for the supplier to totally buy in to the methodology.

Dealers have also taken on the 6 Sigma commitment. More than 165 dealerships have produced more than 1,000 Black Belts to help with projects. Dealers find it amazing that they can share their projects with one another on a Caterpillar website that depicts best practices among the dealers. Even though each dealership is run as a separate business, 6 Sigma has helped give all of them a common feel across the world. Not only are dealerships learning about projects that need to be done in their business, but they’re following the steps of the process and learning which projects to do first. Just as Caterpillar embraced the methodology, dealers have also accepted the idea of making 6 Sigma a top-down methodology that pushes the training and concept down to the workers at the lowest level.

While Caterpillar's Six Sigma push started in 2001, a full four years before it would issue even its first sustainability report, the links between the two efforts are readily evident: In both the CAT approach to Six Sigma efficiency and its sustainability efforts, the drive for waste reduction and efficiency is coming from a very directed and structured approach, one which has its roots in operations.

The intermingling between Six Sigma, operations, production, and sustainability at Caterpillar becomes even more evident when examining the Critical Success Factors [31] statement of its Sustainability Vision, Mission, Strategy:

Critical Success Factors

Culture. Create a culture of sustainability in all our business units and in all our daily work.Progress: We promote our employees’ awareness and understanding of sustainability. We continue to foster a corporate culture of transparency, disclosure and engagement.

Operations. Champion our sustainability principles and contribute to 2020 aspirational sustainable development goals.Progress: The Caterpillar Production System provides the recipe for efficiency and excellence in our facilities. We actively encourage employees to conserve resources and be more efficient. Operating in a more efficient and sustainable manner will reduce impacts on people and the environment, and help us and our customers save money.

Business Opportunities. Identify and pursue business growth opportunities created by sustainable development.Progress: We are actively embedding sustainability throughout our Caterpillar brand portfolio, our new product development process and our technologies. Our business leaders continue to drive growth in sales of products, services and solutions that help customers meet their sustainability challenges. We utilize 6 Sigma methodologies to focus our work and drive measurable benefits.

For one of the world's foremost manufacturers, it would appear a significant portion of Six Sigma enables its sustainability goals, and vice versa. In these types of operations, operating from a place of infused, organization-wide sustainability, it can be very difficult, if not impossible, to determine where "sustainability" ends and "operations" begins.

Efficiency Stagnation

Efficiency Stagnation

Perception of Diminishing Financial Returns in Sustainability Projects

The advent of Lean/Six Sigma adoption in organizations worldwide has also brought with it requisite continuous improvement efforts that analyze virtually every important process and material on a priority-weighted basis. In some cases, the organization undertakes intensive exercises to unearth inefficient processes, then the group elects to engage on the improvement of a handful of those processes by creating task forces. What this has meant for many organizations is that the most inefficient or wasteful areas of the business were likely identified years ago, have received one or more cycles of continuous improvement efforts, and perhaps even the efforts of outside consultants or experts.

This leaves many organizations today in a situation where the cost and effort to take on the next level of new efficiency projects can't be justified by financial measures alone, or cases where the waste is so small as to be inconsequential. In these projects, it isn't even necessarily that the capital needed is an issue, but it tends to be more of a problem of lacking return on investment and overly long payback periods. Many organizations have found themselves in a place where the progress of these higher-level tiers of efficiency projects become dependent on larger trends over time, which may include factors such as:

- Change in fuel or energy costs (i.e., lighting and machine upgrades become more cost effective, or alternatively, less expensive freight opens waste-to-energy as an option)

- Increased material costs (i.e., increased cost of wasted materials)

- Increased cost of disposal (i.e., waste material becomes prohibitively expensive to treat or landfill)

- Change in regulations (i.e., increased regulation requires a different approach, or alternatively, loosened regulations open options before prohibited)

- Significant changes in technology

- New business entries (i.e., a waste-to-energy site opens 30 miles away, making transportation viable)

- et cetera

What we may therefore see is a period of "efficiency stagnation," where the organization may have new efficiency projects queued based on earlier identification, exploration, and scoping (i.e., continuous improvement efforts), but is waiting for something to change to make those programs viable. Unfortunately, those changes don't always work in favor of progressing efficiency, as we have seen some of the same free market forces and commodity prices which helped establish widespread industrial recycling, for example, regress as supply increases. Essentially, recycling's own popularity in industry has made it more difficult for recycling companies to profit, in some cases.

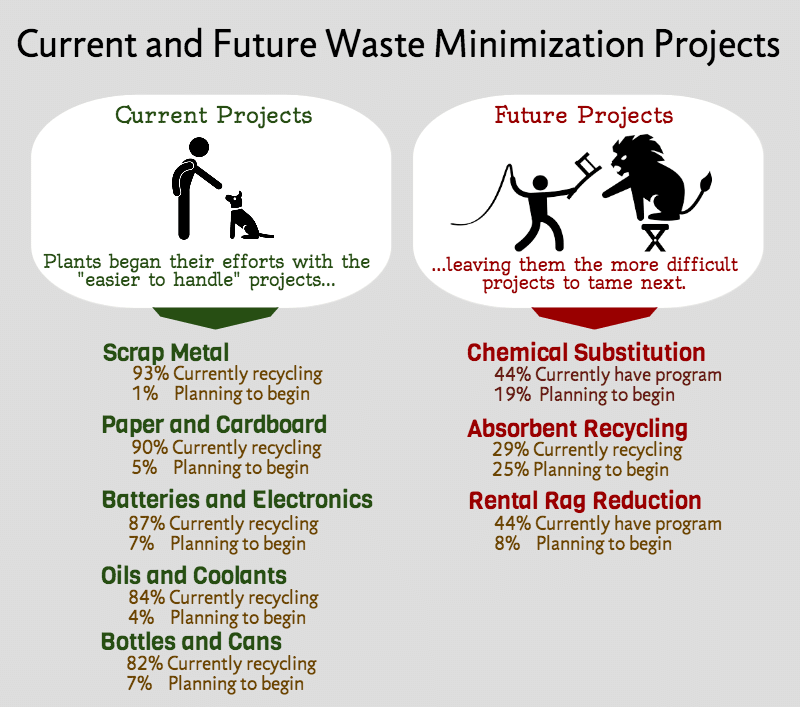

The below is a summary image from a bit of research I did with 304 facilities in the US in 2013, exploring the state of waste minimization. Note the 40+ point drop in adoption rates for the more established "classic" forms of recycling/waste reduction projects to some of the "next level" projects.

An Opportunity for Innovation

What is important for us to note is that this potential stagnation in efficiency projects is not due to a lack of interest on the part of organizations, nor is it due to a lack of capital. Needless to say, an engaged organization with money to spend makes for a fertile ground for opportunity and innovation.

And while we may think that those larger trends cited earlier are the only external tailwinds that can spur an organization to pull an efficiency project from the queue, we must consider an opportunity in the information itself: The fact that these projects are contingent on some external change also signals they are contingent on an organization 1) knowing an external change has happened and, 2) having at least a passing understanding of the interactions between different factors.

Organizations are, by nature, resource constrained. Even the most sustainability- and efficiency-minded organization does not have time to continuously check the state of the art of every process, material, and resource under their purview. So, while a project may have been placed in a queue, it may not be because of the actual state of the situation, but simply the organization's perception of the situation at a given point in time. They may have had limited information on new options or processes, they may have had an incomplete understanding of the situation itself, there may have even been conflict of interest issues in displacing existing vendors or suppliers. Nonetheless, the issue with getting these efficiency projects out of the queue and into action may be as much about quality of information as it is about the actual project to be enacted itself.

Allow me to illustrate:

A few years ago, in talking to plant managers, I started seeing a bit of a trend. When discussing their waste minimization programs and what projects to take on, the discussion always revolved around pounds or tons of waste, but very, very rarely around density. The conversation would go something like this:

Me: "So what's next for your waste minimization program? Have anything on the radar?"

Plant Manager: "Well, we were looking at recycling waste X, but based on our tonnage to the landfill, it looks like it would cost us 10% more to have it recycled."

Me: "What kind of density is it and do you know what you're paying in dumpster rental?"

Plant Manager: (pause) "All I know is that we are paying $90/ton for tonnage, and I haven't dug any deeper because the recycling was more expensive."

It was prevalent enough of a problem I created an Excel-based tool which would allow someone to input ALL of the data related to landfilling a waste, including dumpster rental, tonnage, pull fees, and density (either extrapolated or pulling from EPA-accepted densities of 100 industrial wastes) to understand the full cost of disposal, by prorating all costs by either weight or density. So, if a dumpster was filled with something fluffy, like Styrofoam peanuts, the tonnage would be very inexpensive, but it would be burdened with the full cost of dumpster rental, etc, (which, incidentally, could easily cost twice as much as tonnage). In the case of a heavy material, like brick, it would bear the appropriate costs of tonnage, but only a prorated portion of dumpster rental. It would allow the same calculations for recycling the material, including the cost of any necessary machinery or additional labor.

In the end, it would also calculate payback periods and create an executive summary, as well as calculating cost benefit of source reduction of a waste.

So, only after seeing the full picture, could a facility make the right decision. And in many cases, accounting for the full, real financial burden of landfilling ended up swaying cases heavily toward recycling options. In one example, a recycling program savings had been accounted at $26,000 a year using flawed calculations... with the calculator, those actual savings were shown to be closer to $110,000. In fact, in some test cases, neglecting density could skew actual cost to dispose of some materials by nearly 300%.

In two years, more than 3,000 facilities worldwide of all sizes would use this tool to evaluate the actual costs of landfilling v. recycling to get programs 'out of the queue.'

Why do I mention this?

Because a flawed understanding of just one fundamental portion of the efficiency equation has the ability to keep countless programs on the shelf... and, by bringing new information or insight to the table, those programs can be moved forward in a meaningful way.

Regulatory Risk and the Hidden Cost of Compliance

Regulatory Risk and the Hidden Cost of Compliance

Some Liabilities are Not Recorded on any Balance Sheet

As we continue to discuss the third of the 3Ps, Profit, we may tend to think of those affirmative actions an organization takes which help it turn a profit, therefore helping it remain solvent and sustainable in the long term. This is certainly true. But it is also important to consider how a byproduct of sustainability efforts can invisibly affect an organization's bottom line by reducing or eliminating the costs of regulatory compliance.

Not many organizations have a clear picture of what exactly having to comply with a given regulation costs the organization every year, in terms of productivity, additional capital and equipment, handling areas and disposal contractors, additional training for employees, record keeping requirements, or any other factors. It may be a fun exercise for an otherwise bored actuary to take on, but it is a bit pointless for most operations: why go through the significant complexity of the calculation when the end result remains that the facility still has to comply with the regulation?

In an increasingly competitive international marketplace, operating a business exempt from regulations which may hinder the speed or profitability of peers could be a strategic strength. Unfortunately, the way for some organizations to operate without regulatory oversight is not to reduce the substances or practices being regulated, but to simply conduct those operations overseas in a region with little or no meaningful regulation to start with.

The Hidden Costs of Compliance

So while very few organizations would have a reason to calculate the incremental cost of every environmental or labor regulation they are subject to, in some cases, isolated regulations may be accounted for if they affect operations in a significant way. Despite a concerted effort to understand the cost of complying with a given regulation, evidence shows that organizations may still significantly under-account for the costs of regulations.

In one examination of plant-level financial data of 55 steel mills, Joshi, Krishnan, and Lave (2001) [35] found each was significantly lacking in capturing the total cost of complying with a specific set of new regulations. Emphasis is mine:

The results indicate that visible costs, as reported by these firms’ accounting systems, identify only a minor portion of the overall costs associated with regulatory compliance. For firms in the integrated mill sector, a $1 increase in visible environmental operating expenditure is associated with an increase of $9.23 in total cost (at the margin), of which $8.23 is hidden, and embedded in accounts other than "regulatory costs." Similarly, for firms in the mini-mill sector, an increase of $1 in the visible environmental operating expenditure is associated with an increase in total cost of $10.68 (at the margin), of which $9.68 is hidden. Thus, considering only the visible costs of environmental regulation will seriously underestimate the effect of regulation on cost and profit.

We also conducted structured interviews with corporate-level executives and plant-level accountants from seven steel firms to validate our econometric estimations and to gain insight into such questions as: are the managers aware of the large hidden costs of environmental regulation? What are the reasons for the large hidden costs? What types of decisions are large hidden costs likely to affect? We found that the managers are aware of these hidden costs but seriously underestimate their magnitude. The managers cited several reasons why the accounting system does not identify all environmental costs: difficulty in separating the environmental portion of the incremental costs of materials, utilities, and overheads; problems of aggregation across plants and functional departments; and complexity in separating environmental component of costs of process changes that have multiple objectives.

Our finding that the steel industry suffers from large hidden costs has implications for the design of costing systems in industries facing significant environmental regulations. Gross under-estimation of hidden costs is likely to lead to sub-optimal decisions in managing these costs. Hidden costs may distort variance analysis, contribute to product mis-pricing, and lead to inappropriate product mix, plant closure, and investment decisions. Our interviews reveal examples of these effects. We conclude that managers have under-estimated the magnitude of hidden costs, and our results suggest that they should reconsider the costs and benefits of updating standard costing systems to better track environmental costs.

In addition to the costs of compliance at the Federal level, we can not forget about the highly variable state regulations. Levinson(2001) [36] created a model to index state environmental compliance costs, and found that the variation in compliance costs between states was significant:

Expenditures on pollution abatement in 1994 ranged from 0.5 percent of GSP in Nevada, to 6 percent in Louisiana. While much of this difference is accounted for by differences in the two states’ industrial compositions, the industry-adjusted index for the most expensive state (Maine) remains 1.7 times the national average, and 4.13 times as large as for the least expensive state (Nevada).

A more personal story of the hidden cost of environmental regulation is provided by Drew Greenblatt, President of Martin Steel in a piece he wrote for Inc.(2013) [37]:

When I testified before Congress last winter about the impact of regulatory excess on business, a Congressman posed this question: Don’t the total benefits of environmental regulation offset their cost? After all, the Office of Management and Budget has estimated the regulatory benefits exceed the costs by as much as 16 to 1. Other estimates have found even higher benefit-to-cost ratios, he said.

But the analysis omits one major question: How do you calculate the opportunity cost of thousands of small businesses like mine whose employees are focusing on regulatory paperwork and agency communications instead of serving and finding customers? I’m not sure how those costs are being measured. Is it by the amount of federal employee time and resources put into the effort? Or by the amount of time my employees are filling out forms? (By the way, according to that study that the congressman referenced, the benefits of EVERY agency’s rules outweighed the costs. And the more rules an agency had, the greater the benefits over the costs. Who knew?)

My company’s success relies partly on our ability to reach the 95 percent of consumers who live outside the U.S. But unnecessary paperwork impedes that mission. While we need only three minutes to fill out the requisite form when we ship to Canada or Mexico, it takes us 20 minutes per form when shipping to a non-NAFTA country. If that happened on rare occasion, no big deal, but multiply that step hundreds of times a year and it becomes a mountain. A few years ago, we took a photograph of two Martin Steel employees standing beside the cartons that held our files to respond to government regulations. The stack was three feet taller than they were--and would be even higher today.

Every Risk is an Opportunity for Innovation

As we begin to merge from understanding the pure frameworks and philosophies of sustainability and into the process of layering understandings of how to find opportunities in sustainability, we will continue to revisit and reinforce those earlier frameworks and philosophies. In this case, I'd like us to do a little bit of that now, in consideration of our discussion of regulatory risk and the hidden costs of compliance.

In each of the three examples above–the poor accounting of the cost of compliance by steel mills, the tremendous variance of the cost to comply with state environmental regulations, and the Martin Steel example of compliance paperwork–we need to realize one important point before moving on:

This is why impartiality will be so important in our work together this semester. Do you have a personally-held belief on the situation in each of the examples above as being unjust or overstated, oppressive, regressive, or progressive, believing that regulations go too far or not far enough? Save it for the kitchen table.

When we are talking about finding opportunity for innovation, we have to be able to turn off that biasing part of our brains to be able to recognize the underlying needs of the situation at hand. Those needs may not necessarily fit our organization's competencies, or perhaps they do, but we first need to be able to see without bias:

- Steel mills could use a good accountant and consulting firm to help them capture regulatory costs more appropriately, or a software package to help in creating uniform assumptions of environmental costs. According to the findings of the paper, it's fairly safe to say there are at least 55 steel mills who could potentially need the product.

- The huge variation in state compliance costs offers similar opportunities, from consulting to software to clearinghouses of data to assist in financial projection. I would be curious how organizations with nexus in many states would account for the differences in state compliance costs, if they do.

- Mr. Greenblatt's example of NAFTA v. Non-NAFTA paperwork sounds like a problem many companies could have, and one which occurs with high volume. Are there automation steps, software packages, or regulatory fast-tracks to be benefited from?

Also note that being able to evaluate a situation impartially first does not mean that you suppress your beliefs, ethics, or otherwise... exactly the opposite. It simply means that the first operation is to see, and the second is to layer in our personal perspectives and experiences. Interesting developments and discussions can happen at that confluence of the impartial and the reapplication of our personally-held philosophies. It sounds esoteric, but we will begin to see it in our case discussions as the semester progresses.

Regardless of the needs and potential opportunities created from the need to comply, Porter and van der Linde offer an interesting perspective, and one which relies on data as opposed to a blindly-held belief:

We are currently in a transitional phase of industrial history where companies are still inexperienced in dealing creatively with environmental issues. The environment has not been a principal area of corporate or technological emphasis, and knowledge about environmental impacts is still rudimentary in many firms and industries, elevating uncertainty about innovation benefits. Customers are also unaware of the costs of resource inefficiency in the packaging they discard, the scrap value they forego and the disposal costs they bear. Rather than attempting to innovate in every direction at once, firms in fact make choices based on how they perceive their competitive situation and the world around them. In such a world, regulation can be an important influence on the direction of innovation, either for better or for worse.

[...]

A few studies of innovation offsets do go beyond individual cases and offer some broader-based data. One of the most extensive studies is by INFORM, an environmental research organization. INFORM investigated activities to prevent waste generation-so-called source reduction activities-at 29 chemical plants in California, Ohio and New Jersey (Dorfman, Muir and Miller, 1992). Of the 181 source-reduction activities identified in this study, only one was found to have resulted in a net cost increase. Of the 70 activities for which the study was able to document changes in product yield, 68 reported yield increases; the average yield increase for the 20 initiatives with specific available data was 7 percent. These innovation offsets were achieved with surprisingly low investments and very short payback periods. One-quarter of the 48 initiatives with detailed capital cost information required no capital investment at all; of the 38 initiatives with payback period data, nearly two-thirds were shown to have recouped their initial investments in six months or less. The annual savings per dollar spent on source reduction averaged $3.49 for the 27 activities for which this information could be calculated. The study also investigated the motivating factors behind the plant's source reduction activities. Significantly, it found that waste disposal costs were the most often cited, followed by environmental regulation.

Please read "Toward a New Conception of the Environment-Competitiveness Relationship" by Michael E. Porter and Claas van der Linde [38], from which I cited above. It's an excellent piece, and recounts specific examples of regulatory compliance as fertile ground for innovation.

Sustainability Innovation Leaders - Profit

Sustainability Innovation Leaders - Profit

In this installment of leaders, we will be covering two companies and a philosophy:

- We'll start with Packsize, a unique on-demand box creation system for shipping and fulfillment operations, especially those which are e-commerce centric.

- From there, we'll transition from discussing the negatives of shipping air to the positives of rebuilding heavy iron when we take a look at Caterpillar's Remanufacturing operations.

- And we'll close with a talk from Michael Porter, a leader in business strategy and long-time Harvard business professor, who is discussing the power of profit for social good.

Since Profit is usually covered in depth in public financial filings like 10K (and not GRI), I will be using VISAS to discuss the innovations and how the companies communicate the innovations more so than the sustainability reports.

Packsize

Please watch the following 3:26 video.

Video: Packsize: Packaging for all business types (3:26)

Transcript coming soon

The Insight

Shipping boxes are loaded with inefficiency: either you inventory a tremendous number of different sized boxes and pay a high price per box due to low volumes, or you limit the number of sizes and waste money and material on void filler (i.e. Styrofoam peanuts) and pay unnecessarily high shipping costs due to empty volume. Packsize is a machine that creates perfectly-sized boxes on-demand as an order is fulfilled. Very little, if any, void fill is needed, and shipping costs are reduced significantly.

The Opportunity

With the advent of major online retailers and e-commerce being a major area of growth, parcel shipments reach new records virtually every year. During the holiday season in 2014, FedEx saw a 9% increase in shipments to 290 million, and UPS an 11% increase to 585 million. [40] Despite this massive growth over the past decade, the box itself had remained unchanged and inefficient.

Furthermore, one has to question the sustainability of brands shipping massively oversized boxes [41], as well as how much they are wasting on those boxes.

Vision

Not terribly inspiring, but accurate:

"We are the global leader in On Demand Packaging®. With Packsize as your packaging company, making boxes is easier than printing labels. Smarter packaging means fewer planes, fewer trucks, and less material."

Innovation

The patented software and equipment is the real star of the Packsize offering. They hold multiple patents for the machinery, and it provides speeds sufficient to meet the demands of even high-volume shippers like Staples and REI. It is smart enough to size boxes exceptionally well and with minimal waste. Furthermore, a little bit of business model innovation in that the machines are leased for $1 per year to companies, with Packsize making its money on the cardboard supply (and therefore, actual usage).

The technology, while simple in concept, is a game-changer.

Storytelling

Very little on the emotional side, though Packsize does share some case study videos from satisfied companies. It also does a nice job with some white papers on use cases.

Achievement

They do leverage their client list heavily in most materials, and it speaks volumes: Staples (the world's second largest online retailer), Rubbermaid, GE, Crutchfield, REI, Andersen Windows, and more.

Structure

For what sustainability materials they do have, structure is lacking. It is mostly trivia on packaging waste more than covering how many tons of GHG are prevented from correctly-sized boxes, etc.

The Secret

They're a company making what is a highly sustainable product and using sustainability buzzwords, but they might not really understand sustainability.

Caterpillar Reman

Please watch the following 4:18 video.

Video: Caterpillar Remanufacturing Overview (4:18)

ON SCREEN TEXT: In the next decade, the most successful companies will be those that integrate sustainability into their core business. - Doug Oberhelman, Caterpillar Chair & CEO

For Caterpillar and its customers, sustainability is a competitive advantage and sustainability is what remanufacturing is all about. Caterpillar is a global leader in the remanufacturing business. Our Cat Reman Program supports the cat machine and engine product lines as well as remanufacturing activities at our subsidiaries Solar Turbines, Progress Rail, and EMD. We're setting the pace for the industry and delivering value to our customers worldwide. Customers get a product with the same quality, performance, and warranty as a new product, but at a fraction of the price which really helps reduce owning and operating costs. In short, remanufacturing is good for customers, good for business, and good for the environment. Caterpillar's Reman process reduces waste, lowers greenhouse gas production, and minimizes the need for raw materials. And our customers find new value for products that would otherwise go to the landfill. We remanufacture more than two million components each year. That means Caterpillar recycles an average of 1.94 billion pounds or $880 million kilograms of end-of-life iron each year.

As an example, here's how the process works for Cat Reman products. A customer needs a replacement part for a Caterpillar product. They buy a Cat Reman part or component. The Reman price includes a core deposit which gives the customer financial incentive to turn in the product being replaced. Once the dealer inspects and accepts the old product, also called a core, the deposit is returned to the customer. Now the remanufacturing process begins. The Cat dealer ships the core to one of our core receiving facilities located around the world. We confirm the dealers inspection and refund the cost of the core deposit to the dealer. The core is then shipped to one of our Caterpillar remanufacturing facilities around the world where the remanufacturing work is performed.

First, the core is disassembled into its individual elements down to the level of every individual nut and bolt. Its original identity is lost. Then each element goes through a cleaning process followed by a rigorous inspection using detailed caterpillar remanufacturing criteria. The individual components are salvaged to exact specifications using advanced technologies many of which were developed by CAT Reman. This provides the same quality, performance, reliability, and durability as new while salvaging a significant percentage of the original material creating a sustainable competitive advantage. Elements that don't pass are removed from the process and recycled.

Finally, salvaged and new elements are assembled in the Cat Reman products that include engineering updates. Will fitters just can't match the tolerances, precision, or technology of Cat Reman. Each product is tested to ensure it meets specifications same as new and is assigned a new serial number.

Finally the product is painted and made ready for sale as a Cat Reman product. As a result, our customers can select from a broad portfolio a value-packed remanufactured products. They're as good as when new and as strong as ever. Today we're also remanufacturing products for companies outside of the Caterpillar family which turns our sustainability efforts into an engine for growth. It's good news for Caterpillar, our customers, and the world we share.

The Insight

It all actually started as a favor in 1973. Ford, a major customer, asked Caterpillar to supply it with rebuilt truck engines. "It was something we had to do," according to Steven L. Fisher in a 2005 Bloomberg article. [43]

The real insight would come when Caterpillar realized how profitable the remanufacturing division could be.

The Opportunity

To make profit multiple times on the same Caterpillar part while providing customers with outstanding service and a factory warranty. An engine connecting rod can be rebuilt up to seven times during its life, and CAT Reman will turn a profit on every single one of those "seven lives" while keeping that iron out of a scrap yard or landfill.

To give you a feel for the size of the Remanufacturing division, it remanufactured 500,000 tons of equipment from 2004-2014 [44], and revenue is predicted to grow at at roughly 20% annually.

Vision

From "The Benefits of Remanufacturing":

GOOD FOR CUSTOMERS

Cat remanufactured parts and components provide same-as-new performance and reliability at fraction-of-new costs—while reducing the impact on the environment. And over-the-counter availability gives customers more options at repair and overhaul time. The results are maximum productivity and lower costs.GOOD FOR BUSINESS

The remanufacturing program is based on an exchange system where customers return a used component (core) in return for our remanufactured products. Reman options are one more way we support our customers and help lower owning and operating costs.GOOD FOR THE ENVIRONMENT

Caterpillar is a global leader in remanufacturing technology, recycling more than 120 million pounds of end-of-life iron annually. Because we are in the business of returning end-of-life components to same-as-new condition, we reduce waste and minimize the need for raw material to produce new parts. Through remanufacturing, we make one of the greatest contributions to sustainable development—keeping nonrenewable resources in circulation for multiple lifetimes.

Innovation

While the program may seem straightforward, the logistics of returns, fulfillment, and refunds, let alone the thousands of remanufacturing processes themselves, are daunting. Caterpillar is famously tight-lipped about its manufacturing processes, but to be able to resurface and rebuild parts with service lives in the tens of thousands of hours is an engineering achievement, however it is accomplished.

Storytelling

Caterpillar gives the Reman division significant airtime in both its Sustainability Report as well as its core marketing, sharing stories of both success and satisfied customers.

They are especially proud of the fact that their "take back" percent, that is, the percentage of parts that are returned for remanufacturing, hovers between 93% and 95%.

Achievement

They capture achievements in a few different ways throughout their CSR and marketing materials, and all are illustrative: lbs of EOL material remanufactured and placed back into service, % of total parts remanufactured, etc.

Structure

They do a solid job of making sure that the emphasis they place on the Reman program in their sustainability program is reflected in their sustainability goals in a meaningful way. In fact, two of their nine major sustainability performance measures are Reman specific indicators.

The Secret

Caterpillar now considers remanufacturing in the product design process so that it may become ever more efficient... and profitable.

Michael Porter

Please watch the following 16:24 video. If the video is not displaying on the page, please view it on the Ted website [45]. A transcript is available on the external site as well.

Video: The case for letting business solve social problems (16:24)

Overall

While I do find that Porter makes quite a few good points in this lecture, I tend to be more of a fan of his writings on the topic (namely his paper you read on the last page).

Closing Remarks

Closing Remarks

"I haven't got it yet, but I'm hunting it and fighting for it, I want something serious, something fresh—something with soul in it! Onward, onward."

-Vincent van Gogh to Theo van Gogh, January 3, 1883. [50]

Finding our Palette

The intent of our last three Lessons on the 3Ps–Planet, People, and most recently, Profit–is not just to lay the foundations of our understanding of sustainability as it is practiced today, but to get a feel for just a fraction of what our "palette" might look like. Not that we are necessarily even sketching at this point, but we are beginning to immerse ourselves in what is available to us in creating sustainability-driven innovation. By looking at the underpinnings as well as some leaders in each realm, we may begin to see how others have used their palettes and the deliberate selections they have made in creating their works. As we have seen, each organization will have various strengths, competencies, and economic moats, all of which may be leveraged in creating innovation works which are sustainable, defensible, and ownable for the brand.

In understanding Profit, we understand one of the essential components of any innovation we seek to create in the sustainable space. Realistically, if we seek to create businesses and opportunities from these innovations, Profit, or more appropriately, the potential pathways to profit, will be of significant concern. Even for NGOs and non-profits, it is undeniable that the revenue must be there to be able to do further good works, whatever they may be. In our own thoughts and in discussions with others, we must remember that for sustainability to be truly sustainable, there must be profit. Whether a specific initiative or a sustainability program as a whole, the profit or value must be evident. Otherwise, that initiative or program is living on charity and borrowed time.

Adding Depth and Theory to our Work

My hope is that as we progress through our time together, you will begin to find your voice and your philosophies and begin to refine your approaches to both innovation and sustainability. I have personally known innovators of all types:

- the extremely deliberate, experiment-driven engineer

- the brilliant and emotional artist

- the impatient and anti-authoritarian rogue

- the precise and organized project manager

- the identifier (and funder) of innovation in others

...and they are all equally effective in their own ways. What you may find is that you may work one way in your daily work, but when you engage in innovation and emergent work, you tend to take a different approach. Great, go with it, and I hope that we will see that approach and flair–whatever it may be–in your writings and discussion.

While we have spent the course thus far primarily immersing ourselves in the "colors" of sustainability, the close of this Lesson marks not necessarily a transition as much as the addition of another dimension of our work: theory and analysis. We will begin to not just discuss current and emerging trends, but to dissect innovations and break them into their component parts so that we may understand them more deeply. Specifically, in the next Lesson, we will examine the available tools for finding opportunities in sustainability, in essence, identifying clusters of interest.

If you're wondering about the lead image on this page, it represents the percentage of colors van Gogh used in his 28 most famous works. You may see a bias toward his trademark rich yellows, golds and browns, but in the act of abstracting color and taking a more critical approach, we see he also used quite a bit of varied color in his pieces.

This lies at the core of what we will be doing next, going beyond admiring the works and into understanding how they are created and composed.