Lesson 6 - Other Market Failures

Lesson 6 Overview

In the previous lesson, we talked about the first and most common violation of perfectly competitive markets, that being market power. As you are aware, there are three other assumptions of perfect competition that can be violated, leading to market failure of some degree. In this lesson, we will examine a couple of other types of market failure, those being violations of the assumption of free entry and exit as manifested in the form of barriers to entry into a market, and how market players can use imperfect market information to distort market outcomes. We will also look at a special case of monopoly, where having only one supplier actually makes sense from an economic efficiency standpoint, and how society deals with such monopolies.

What will we learn?

By the end of this lesson, you should be able to:

- list and explain the several types of barrier to entry as outlined in the next section of this lesson;

- describe just how it is that natural monopolies can exist;

- describe the negative outcomes that derive from a natural monopoly;

- explain the methods that societies use to deal with natural monopolies;

- list and describe the aspects of information market failure described in this lesson;

- understand and explain when and why firms will use information market failure to their advantage.

What is due for Lesson 6?

This lesson will take us one week to complete. Please refer to Canvas for specific time frames and due dates. There are a number of required activities in this lesson. The chart below provides an overview of those activities that must be submitted for this lesson. For assignment details, refer to the lesson page noted.

| Requirements | Submitting Your Work |

|---|---|

| Reading: Most of the reading in this lesson will be rereading of selected material from Chapter 11 of the text, "Price Searcher Markets with High Entry Barriers." | Not submitted |

| Lesson Homework and Quiz | Submitted via Canvas |

Barriers to Entry

Reading Assignment

This material is discussed in Section 9.1 [1] of the text, in Chapter 9. You should have read Chapter 9 for the previous lesson, so this will be review for you.

In the previous lesson, we spoke about monopolies and oligopolies. These are markets where there is only one or are only a few sellers, and therefore, suppliers in these industries are able to earn greater than zero economic profits by charging at prices above the point where .

In a competitive market, this would be a signal to other suppliers to enter the market and compete for business with other suppliers by driving price down to marginal cost, and economic profits down to zero. In a monopoly, this does not happen. This is one of the violations of the assumption of "free entry and exit." Here we will talk about "free entry," or the ability of firms to enter a market. Another manifestation of this assumption is the notion of "free exit," meaning that an individual is free to choose to not participate in an economic transaction. When people are negatively and involuntarily affected by some economic transaction they do not willingly participate in, we have the issue of "externalities." This will be addressed in the following lesson.

As I said in the previous lesson, there is a very limited set of reasons why monopolies can persist. These are:

- A monopoly has government protection.

- A monopoly involves having total control over a limited-supply good.

- A natural monopoly exists, where it is economically efficient to have only one seller.

The third of these types of market, a natural monopoly, will be talked about in the next section of this lesson. In this section, we will talk about the first two types of monopoly.

Economists generally believe that market forces are always powerful enough to break a monopoly. For a monopoly to be able to stay in existence over time, it must need some protection from market forces, and such protection can only typically come from government. In most cases, government generally acts to try to reduce monopoly power, since we demonstrated in the past lesson that monopolies are detrimental to economic efficiency, as well as hurting equity. Put in simpler words, we don't like monopolies for a couple of reasons: they tend to concentrate wealth into the hands of already wealthy individuals, and they hurt the total wealth of a society by causing unsatisfied demand to exist - there are people who are willing to purchase a good at a price higher than the marginal cost, but are unable to because monopolists refuse to produce the goods, instead restricting output to the point where .

So, governments generally discourage monopolies. At the Federal level in the US, this is typically performed by the Federal Trade Commission, or FTC, which is a branch of the Department of Justice responsible for maintaining fair and open markets. Another group that polices markets, specifically in the energy arena, is the Federal Energy Regulatory Commission (FERC). I strongly suggest that you take a look at the FERC website [2] if you are interested in how the energy industries are regulated at the Federal level. There is a wealth of information available at that website. If firms act in ways that are deemed to be detrimental to competitive markets, they can be sued, fined, or punished in other ways. One famous case involved the Department of Justice suing Microsoft for being an illegal monopoly, and seeking to break Microsoft up into three companies, two operating system developers, and one applications developer. Microsoft was able to defeat that lawsuit. Another famous case was the breakup of Standard Oil in the first decade of the last century. I suggest you read about the Standard Oil case [3].

However, despite the fact that government generally fights monopoly, there are some instances where governments either allow, encourage, or even protect monopolies. These, and some other barriers to free entry in a market, are described below.

Types of Barrier to Entry

Legal Restrictions

Governments sometimes restrict competition, either from domestic or international competitors. This is sometimes done to help develop a native industry where none existed, sometimes for nationalistic reasons, and sometimes because a firm has lots of influence with the government. For example, the United States restricts the importation of sugar into the country, protecting from global competition the 800 or so firms in the US that make sugar. This harms American citizens who consume sugar by making it about twice as expensive as in neighboring countries. It also drives candy manufacturing to Canada, because the cost of making candy is cheaper there, and there are few barriers to the entry of candy into the country.

Licensing Requirements

In many cases, in order to enter a profession, a government either sets licensing requirements, or empowers some other body to set such conditions. In many cases, this is generally approved of by the public: we like knowing that our doctors know what they are doing, and that our accountants are certified as competent. However, such rules apply to many other professions. In many states, if you wish to buy a casket to bury a deceased relative, you have to buy one from a funeral director, and to become a funeral director you have to get a license. The awarding of licenses is typically controlled by commissions that are dominated by members of the funeral profession. Therefore, an industry is able to restrict free entry by competitors, enabling the incumbent members to set prices higher than in a free market. The same is true of flower arrangers, or hair cutters, or tour guides in many states. The industry in question will have licensing commissions, whose role is nominally to protect the public from fraud or incompetence, but which, in reality, merely serve to restrict entry and stifle competition.

Another example of this is taxi commissions. In most cities, if you wish to operate a taxi cab, you need a license, often referred to as a "medallion." In most cities, the number of medallions available is limited. For example, in New York City, there are 13,000 taxi medallions [4] available. Many people believe that this is far too few for a city the size of New York, and one of the effects is that a lot of unlicensed "gypsy" cabs operate, completely out of the view of the authorities, in violation of regulations.

Patents

A patent is a government license to have a monopoly for a certain length of time in a certain good. Patents raise the price of a good, but are felt necessary to promote invention and technological progress.

The above paragraphs refer to methods by which government erects barriers to entry. Below are some other methods that can be employed by firms, that are of various levels of legality. In many cases, these behaviors will be challenged by governments, but it is not always easy to observe and verify that such actions are taking place, and, if they are, whether they cross the line from "aggressive business behavior" to "illegality."

High Fixed Cost versus Small Margins

In many industries, you have to spend a lot of time and money before you are able to sell anything. The longer into the future the potential profits are, the more uncertain the return, and the more uncertainty, the greater profit required. Many such industries fall into the category of "natural monopoly," which will be addressed in the next section.

Predatory Pricing

This is connected to the above point: a firm that is established has often recovered its capital costs (its buildings and machines are paid for). This means that it can lower its price, and it will not be harmed as much as a competitor with high capital costs. So a predatory pricer will lower his price to drive his competitors out of business. In reality, this does not happen often, and economists believe that it generally does not work. But sometimes the threat of predatory pricing is enough to stop a competitor from entering a market.

Excess Production Capacity

This is also related to the above point: an existing monopolist will usually keep some spare production capacity. If a new firm enters, the old firm will increase production, thus driving down the price and making it less profitable for both firms. This is tied in with the idea of economies of scale.

Bundling

Also called “tying,” this means selling several items as a package. Perhaps the best example was Microsoft adding an Internet browser for free to their operating system. This destroyed the previous market leader, Netscape, who used to sell their browser software.

Brand Loyalty

As mentioned in the monopolistic competition section, every firm would like to have a monopoly, and the legal way to get this is through product differentiation from advertising. If you develop a valuable brand, it is difficult for people to compete – imagine launching a new drink to compete against Coca-Cola.

Natural Monopoly

Reading Assignment

Please reread "Characteristics of a Monopoly" on pages 210-213 in Chapter 11 for this section.

In a competitive market, we expect firms to compete with each other until the point where marginal cost increases to match the demand curve at the equilibrium point. For this situation to be able to occur, we make the assumption of upward-sloping supply (marginal cost) curves. This is a reasonable assumption to make, because as production of some good increases, the cost will increase because we have to compete with other goods for consumption of the inputs. That is, if we want to open a factory to make more detergent, we will have to hire workers, and assuming that we have something close to full employment, to get those workers, you will have to offer them higher wages than what they are receiving from their existing jobs. Simply put, we can reasonably expect supply curves to be upward sloping.

But sometimes, they are not. There are cases where the marginal cost, that is, the cost of satisfying one more customer, is lower than the cost of servicing the previous customer. In such a case, the marginal cost curve, and thus, the supply curve, will be downward sloping or flat over the relevant range of production.

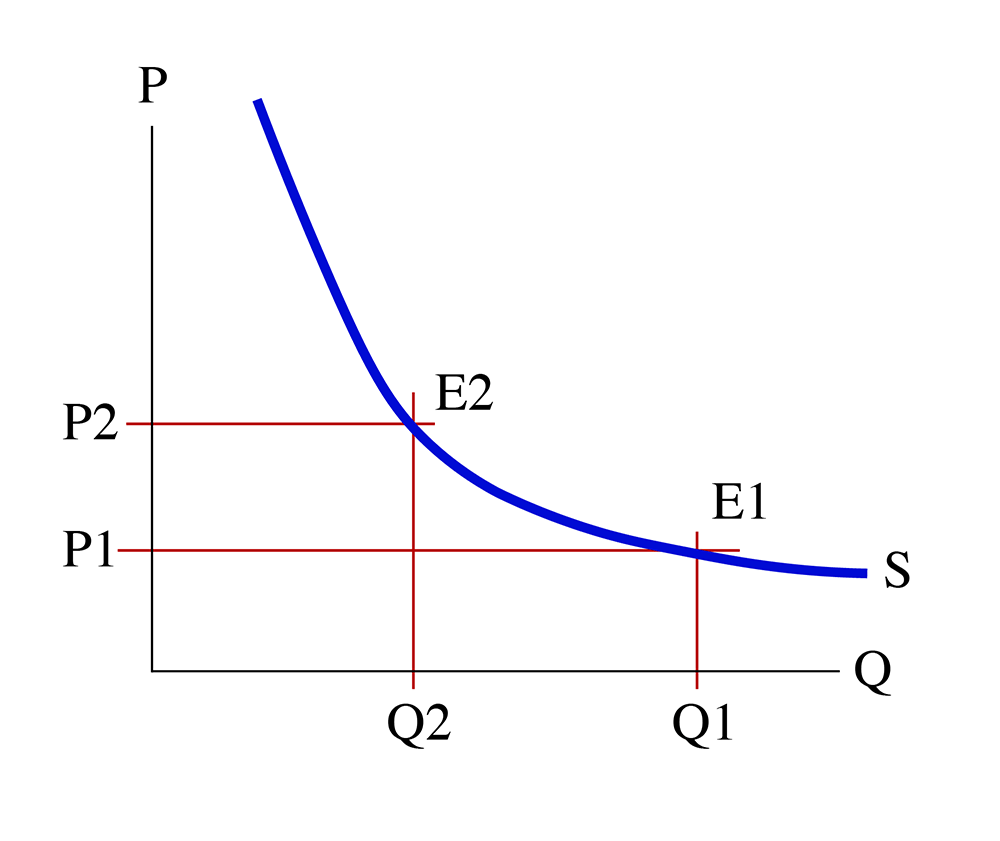

This is called a “natural monopoly” because it is economically efficient for there to only be one supplier. The following diagram can help to illustrate just why.

I should comment here that the textbook lumps natural monopoly in with other barriers to entry, and while it can potentially be thought of as a barrier, it is not one that is created by a market-power-seeking firm. Instead, it is a characteristic of a certain type of market - one with high capital costs and low marginal costs.

Given the downward sloping supply curve, and ignoring the demand curve for a minute, let’s say we have an equilibrium at point E1, which corresponds to quantity Q1, and gives us price P1. Let’s assume this is a monopoly equilibrium, where Q1 represents the entire size of the market – it represents everybody who wants to buy the good.

Now, let’s imagine that this was a duopoly market, where there are two suppliers. We can assume, for simplicity, that each seller in the market has exactly half of the market. This corresponds to the equilibrium E2 on the above diagram, which gives us quantity Q2 and price P2. We can assume the , and that each of the two firms supplies Q2 of the good in question.

Do you see the problem? If we have one firm only, the marginal cost of supply is P1, which is lower than the duopoly price, P2. This means that having two firms in a market ends up with the firms having to charge a higher price than if only one firm existed. In this case, it is efficient, or “natural,” for there to only be one firm in the market. This is why declining-marginal-cost industries are called natural monopolies.

What types of industries have this type of structure? Well, generally, industries that have very high capital costs, and comparatively low variable costs. This means that to be the first entrant, you have to spend a large amount on fixed costs, but the cost of servicing an extra customer is very low. Some typical industries would be the delivery of telephone services, or natural gas, or electricity, or cable television. These industries are typically referred to as “utilities,” and they require the development of large infrastructures to serve the customer base. For example, if you have a natural gas distributorship, you have to build a large network of distribution pipes and valves covering an entire city. This represents a pretty massive capital (or fixed) cost component, but the cost of servicing a new customer is very small compared to that.

Now, imagine that this was a competitive market. If there was to be competition between different natural gas suppliers, then there would have to be two sets of distribution pipes. Each firm would have to spend a lot of money, but then compete for the same size of customer base. Each firm would have to spend the same amount of money, but have half of the size of market to try to recover their costs from. Therefore, it makes sense for there to only be one firm in each city – it would be economically inefficient to have two competing natural gas distribution grids, just as it would be inefficient to have two redundant electricity grids, or two telephone grids, or sets of water distribution pipes, and so on.

The Problem of Natural Monopoly

Because natural monopolies tend to be utilities, which are services like gas, electricity, water, and telephones, which the public generally holds to be necessities of life, we are not comfortable allowing these firms to charge monopoly prices (i.e., the pricing where ). Because these are staples or necessities, the demand curve for these goods is very inelastic – it is very steep. This means that the monopolist price would be much higher than the free-market price, and a large volume of people would be denied basic necessities of life. Instead, we use the power of government to regulate prices in these markets.

The normal avenue for regulation of natural monopolies is the public utilities commission. These exist at the state-level in the United States, and at the national level in many other countries. Utilities commissions are given the task of making sure that utility companies make enough money to stay in business, but not enough to enjoy monopoly profits. They make sure that everybody is served, and served well, in theory. Since utilities are monopolies that are not subject to market forces and competition, they have little pressure to be responsive to market forces, which means that they do not have to treat their customers well, because their customers do not have the ability to switch to a different supplier.

In an ideal, perfectly competitive market, we expect price = MC. So, if we were the government power, we might want to regulate the utility to this point. Unfortunately, in a natural monopoly, this would lead to failure of the firm, because of the notion of declining marginal cost. If the firm was paid the marginal cost of the last unit sold for all units (that is, if the law of one price were to apply), then they would lose money on every unit sold, and, inevitably, fail. Another way to say this is that the marginal cost is always lower than the average cost, because the cost of the next unit is lower than all of the previous units made. For a firm to be able to survive in a natural monopoly, it must be able to charge at least the average cost.

Therefore, the goal of the utility commission is to make sure that a utility is able to charge no higher than average cost. However, most utilities are private companies (although some are owned by local governments in many parts of the world), and as private companies they strive to maximize profits. Typically, a private utility will file what is called a “rate case” to a utility commission, which is basically a statement of what the utility needs to earn in order to stay in business and ensure reliable service. It is the role of the utility commission to examine the rate case and see if it believes that the utility is exaggerating its costs. One of the problems of regulating a utility is that they usually are allowed to earn a certain percent accounting profit on their capital base. That is, the larger the capital base (the more buildings and pipes and power plants, and so on) that a utility owns, the more money it is able to earn. For this reason, utilities tend to be “over-capitalized”- they build more capital than would exist in a competitive market.

Another of the benefits of competition is that it drives innovation and efficiency: firms are always trying to come up with smarter and cheaper ways of doing things. While such actions lead to private gains in the near-term, they tend to be beneficial to society over time, as firms make profits and reinvest these into other productive uses. In a monopoly, these pressures also exist to some extent – if a firm can be smarter, it can make more money at the same market prices - but it is totally absent in a rate-regulated natural monopoly, since firms are allowed to earn a certain amount of money by the Public Utility Commission and any extra money they earn must be returned to the public. While such a result is good for the public, it is not for the utility, and therefore, the utility is unlikely to be particularly innovative or efficiency-driven.

The biggest issue in utility regulation today is the question of how to incentivize innovation in utilities, especially when public watchdog groups keep a close eye on what happens at utility commission meetings and protest loudly if they think the commission is allowing the firms to earn too much money, or include too much into the rate base. If a utility wants to spend any money on research and development, they must get approval from the commission, which will then allow the firm to recover the costs of that research. This means that electric or gas or water rates will be higher than they would be without the R&D spending, and members of the public complain if their rates go up. In many places, utility commissioners are elected by the general public, and they usually wish to be re-elected. This means that they want to keep the public happy, and they best do this by keeping rates low. So, we are stuck in a circle of bad incentives that leads to technical stagnation and a lack of innovation.

We will spend quite a bit of time talking about this when we look deeper at the issue of government failure in a few weeks.

Former Natural Monopolies

The above statements about lack of innovation and competitive pressure do not mean that natural monopolies are immune to technological innovation that weakens their market power. Instead of having multiple firms compete to provide a single service, instead, we now have competing technologies attempting to provide the same service. The most obvious example is that of telephones. It used to be that the telephone system, or at least the part of it from the end user to the phone company’s switching and transmission points, was fully hard-wired. The local phone company had to build a network of cables connected to every house, usually at very high cost, a cost that could only be recovered by either charging monopoly prices or having regulated profits. It was a classic natural monopoly, and one that is government regulated or government-owned in many parts of the world. However, new technology was developed that allowed that last piece of wire between the customer and the phone company to be replaced by radio signals. Thus, we have the cellular phone, and competition with the land-line telephone. People no longer have to rely upon the old-fashioned phone company for their voice communications needs. The same is true of cable television and satellite TV, and now we can get Internet services delivered by the cable company or the phone company or the cell-phone company. Thus, the list of markets that can be classified as natural monopolies has shrunk in recent years. We have yet to find competitive alternatives for electricity, natural gas, and water, and markets for these products remain tightly regulated.

Information Market Failure

Required Reading

Please read pages 103-106 in Chapter 5, the segments entitled "Potential information Problems" and "Information as a Profit Opportunity." This is in the chapter entitled "Difficult Cases for the market, and the Role of Government."

Perfect information is one of our assumptions of perfectly competitive markets, and it is easy to see that this assumption is perhaps the toughest one to make, simply because perfection is something that does not exist. Information can have many aspects in a market setting. The foundation for our analysis of demand in markets is the idea that people are able to place value on the consumption of goods, on understanding the amount of happiness they will obtain from the economic decisions they make. Since the realization of many of our economic decisions takes place in the future, and because the future has an unknown component, it is basically impossible for us to have perfect knowledge without perfect foresight – and that is something we do not have, and cannot have.

However, as a market failure, this is not something we can correct. We can, as individuals, educate ourselves about the world and what sort of outcomes we can come to expect. We can gain wisdom and insight, but we can never tell the future with certainty. Thus, we will consider this issue further. It is merely a manifestation of the nature of our existence and the linear nature of time.

Instead, we need to concern ourselves with information that is knowable, but the lack of knowledge by one or another party in an economic transaction causes a loss of wealth to society.

Some markets have close to perfect knowledge of present information. Perhaps the best example is the market for shares of widely traded public companies at places like the New York or London stock exchanges. The shares are all homogeneous – one share is exactly the same as another, the prices are readily available, in real-time, to anybody who is interested, and there are many, many people studying the activity of the companies that are being traded. Because they are publicly traded on stock exchanges, these companies are required to release a lot of information to the public about their business activities, their profitability, their debt levels, and so on. Generally, a person buying a share in a large public company like IBM or General Electric or Exxon knows or, at least, has the ability to know, about as much as anybody else in the market for the share in question.

There is one situation where somebody might know something about a company that the general, investing public does not: when a person is an “insider,” and has some non-public knowledge about the future of the company. A manager or director of the company may know that they are in the process of planning a takeover of another company, or are being taken over, or are about to suffer a large loss due to some non-public event. The announcement of such pieces of information can have significant effects on the price of shares of these companies. Thus, insiders can profit greatly by buying or selling stock using information that is not available to the general public. This is what is referred to as an “information asymmetry.” For this reason, insider trading of stocks is highly regulated in many countries. Insiders – managers and directors – have to make public record of their stock trades, and if a material event happens that they can reasonably be expected to have had inside information on, the securities authorities will examine the history of their trades to make sure that they did not profit from that knowledge unfairly. If they are found to have done so, they can be severely punished. In other countries, for example, Germany, the securities authorities make sure that all insider trades are publicized immediately, so that the general public can mimic them. The authorities in countries like this assume that this is a better way to disseminate information about what is going on in markets and in industry. If insiders are making big moves, and people can see them, the market will assimilate that information quicker than it otherwise would. At least, that’s the theory. If you go ahead and study finance, this is what is called the strong form of the efficient markets hypothesis, about which there is a great amount of disagreement in academic and professional circles.

The last type of information market failure concerns another type of information asymmetries: that about products or services being sold. It is not hard to realize that, typically, a seller of a product knows a great deal more about that product than the buyer. Sometimes, a seller will use this to his advantage by not telling the buyer something meaningful and important about the product. This is sometimes referred to as getting “ripped off.”

When will a seller take advantage of such a situation and “rip off” a consumer? The short answer is: when it pays to do so. More specifically, there are some conditions:

- When you can’t find out that you are being cheated until after the purchase is made, and

- When you can’t punish them once they’ve cheated you:

- When you only make a single purchase from the seller. For example, most people only purchase a house a few times in a lifetime and very rarely more than once from the same seller.

- When there is only one seller. If you feel like you’re getting ripped off by the power company or the only gas station for 20 miles, you cannot easily take your business elsewhere.

- When getting cheated is a small enough loss to not change your preferences.

- When you will never find out if you have been cheated. One example of this is people undergoing unnecessary surgery. This why they say you should always get a second opinion.

So, summing up, sellers will have an incentive to cheat buyers when buyers cannot adequately punish sellers.

Consumers can also take advantage of suppliers — moral hazard. The best example of this is insurance:

- a) Insurance companies agree to pay your damages after an accident.

- b) However, they do not control your behavior, and you have incentives to be risk-loving, knowing your damages will be paid.

Another example is academic integrity:

- a) Most teachers believe that you hand in your own work and don’t go to great lengths to certify that what you hand in is yours.

- b) However, they cannot control (or costlessly discover) whether you have done the work yourself, or copied from a friend.

Of course, when insurance companies (or teachers) catch you, consequences are usually significant.

Correcting Information Market Failure

In this case, there are private as well as public (governmental) solutions:

- Trade Organizations: If a company misbehaves, their reputation will be hurt and the trade organization will cease to support them.

- Consumer Organizations: Publications like Consumer Reports independently monitor companies’ performance and keep consumers informed.

- Anti-Fraud Legislation: If you can prove a company cheated you, they will have to pay restitution to you and prohibitive damages to the government.

Summary and Final Tasks

In this lesson, we looked at some of the other types of market failure that can exist. Firstly, we talked about one of the manifestations of the violation of the assumption of free entry and exit, that being the way in which some incumbent sellers in a marketplace try to erect barriers to entry into a market, which helps reduce the amount of competition a firm faces, whether it is a monopoly or not. There are various barriers to entry, some supported by government, some illegal, and some perfectly legal. We then talked about natural monopolies, which are typically utilities, in which it makes sense from a standpoint of economic efficiency to have only one supplier in each market. The last section was about the violation of the assumption of perfect information. We spoke of some ways that asymmetric information can be used to gain an unfair advantage in a marketplace, and when and why this information can and will be used.

Have you completed everything?

You have reached the end of Lesson 6! Double check the list of requirements on the first page of this lesson to make sure you have completed all of the activities listed there.

Tell us about it!

If you have anything you'd like to comment on or add to the lesson materials, feel free to post your thoughts in the discussion forum in Canvas. For example, if there was a point that you had trouble understanding, ask about it.