Preparedness

Preparedness

The goal of the preparedness stage of the disaster management cycle is to enhance people's capacity to respond to natural hazards and recover from a disaster. The basis of preparedness is planning, whether that planning takes place at the household, local, state, national, or international level. Thus, policies from a local to international scale that guide sound hazard and disaster planning are essential. Emergency planning and communication of plans for their successful execution when a hazard occurs, happens at many levels of society, from the federal level down to the individual. Therefore, for organizational units including state, county, and city governments, to schools, universities, hospitals, and many other organizations, a clear plan is essential.

Insurance Challenges

Insurance Challenges

Insurance coverage for homeowners in hurricane prone areas is becoming one a major policy challenge. As it turns out both instructors have their own insuance nightmare stories to tell.

The recent and ongoing cost increases for homeowner’s and flood insurance coverage in coastal Louisiana (including metro New Orleans), coupled with collapse or relocation of some insurance companies, is negatively impacting ordinary, working people who live in the area. Dinah’s experience may be “average” compared to her neighbors, some of whom have suffered much greater heartache and loss following Hurricane Ida in 2021. Ida hit the Louisiana coast as a category 4 storm, wrecking the Gulf town of Grand Isle and leaving a wide swath of flooding and wind damage in its wake as it traveled inland. Jogging close to New Orleans, it wreaked havoc in the western suburbs of the city, leaving tens of thousands of damaged roofs, not to mention cutting power and water for weeks. Then came the insurance nightmares, playing out over the next couple of years. Dinah had a homeowner’s policy with a company that left Louisiana because of Ida’s losses. Although this insurance company did cover the cost of the repairs, including a new roof, a new homeowner’s policy had to be found. As of 2023, the cost of the new homeowner’s policy is approximately 3 times the cost of the original one at over $3,000 annually. Many families cannot afford these policies, and some go without. This results in neighborhoods sporting blue tarps for years after a storm as repairs are unaffordable for many families.

Meanwhile, flood insurance has increased steadily each year (FEMA's updated Risk Rating 2.0 is allowed to impose an 18% annual increase to existing policies). Dinah’s house is in flood zone X and does not require a flood insurance policy, but recent experiences in Louisiana mean it is wise to carry flood insurance in this location. The house is a few blocks from the Mississippi River levee and close to much lower ground and flood zone AE. Dinah’s family also has a small home in coastal Mississippi (flood zone AE), built recently and elevated to 20 feet (3 feet above the required base flood elevation). Flood insurance on this property under the new National Flood Insurance Policy is $4,000 annually. Again, this is a modest house and built with flood mitigation in mind. Other properties are much more costly to insure or are uninsurable because they do not meet minimum elevation requirements. In some cases, families use cash to purchase homes and go without insurance. It is clear as Dinah looks around and talks to neighbors that these increasing costs are having a deep impact on the housing market, changing what were previously modest neighborhoods in coastal areas into places only the wealthy can afford, and many properties are bought by companies that make rental money from them. This is happening all around the coastal areas of the U.S. and impacting millions of people.

Tim’s insurance nightmare started after hurricane Fran sent a 150 foot red oak tree onto his Chapel Hill house at 2AM on September 6th 1996. The tree caused extensive roof damage and water damage in the house. Ceilings were wrecked and carpet was damaged. He contacted his insurance companies, one of the largest insurance companies in the country, and they came out to the house within days and promised to help restore the damage. It was a shock when a letter from the adjustor arrived with estimates of what the company would pay. 54 cents a square foot for ceilings to be repaired, a few hundreds of dollars for the roof. This was insult to injury for Tim and his family who had endured to trauma of a massive tree hitting their roof followed by 10 days without power in sweltering heat.

This anecdote is sadly very common for home and business owners who have been impacted by storm damage and the situation seems to be getting worse as coastal areas have become increasingly developed and storms more devastating. In fact, insurance companies themselves have been faced with major financial losses resulting from major hurricanes. Homeowners’ premiums have risen sharply, and in several cases, insurance companies have left states such as Florida and Louisiana because business is not profitable. This leaves states in a real bind as these two videos show.

Video: Florida Faces Insurance Crisis From Hurricane Ian (7:56)

the initially insurance carriers will come in we'll probably have somewhere between 20 and 25 carriers ago and they'll probably set up an RVs and they will start writing checks initially that will be living expense money this will be the dollars just to help people go find a place to live sustenance dollars uh then you'll be signed up where adjusters will come and inspect the damage sounds easy but it is not so easy a real estate data company estimates 28 to 47 billion dollars in losses from that hurricane are expected it is the costliest Florida storm since Hurricane Andrew back in 1992. many hard hit by the hurricane simply don't have the insurance they're going to need to rebuild the New York Times reports in the counties whose residents were told to evacuate just 18.5 percent of homes have coverage through the national flood insurance program as our own Kerry Sanders has more on how Florida insurance companies are facing their own massive challenges they can't afford to stay in business anyone with a mortgage in a flood zone is required to carry Federal flood insurance but wind damage is covered by your homeowner's policy in Florida six insurance companies have claimed insolvency just this year homeowners complain those that are still in business here have jacked up premiums I'd say probably about a 30 increase for myself others I've seen them you know rise 50 percent 100 percent and some have just been canceled altogether Insurance Crisis in Florida the hardest hit counties in the storm's path experienced huge population booms in the last three decades joining us now to discuss Alex Harris climate change and hurricane reporter for the Miami Herald and our dear friend David Jolly a former Republican congressman from the state of Florida who is fortunately safe in Pennsylvania tonight Alex just how complicated is insurance in Florida right now is it that they are jacking their premiums or can they just not afford to stay in business given the amount of storms and damage that state faces yeah the insurance Market is really tough in Florida right now we have uh all of these companies going Belly Up and flipping their uh their clients over to Citizens our state friend insurer of Last Resort and that's stressing people out but also I mean these companies are forced to raise these rates because of things like fraudulent uh claims and assignment of benefit fraud there's a lot going on in the financial Market insurance right now and Florida isn't the only place struggling but up until this week one of the reasons we weren't struggling was that we hadn't had a storm and now we expect that to be a domino that really sets off some crisis over here and David you've been a How do you solve for this beneficiary the Florida real estate market has been hot hot hot you've got pretty LAX zoning laws there and things are built in all sorts of areas that maybe shouldn't be so how do you solve for this especially the insurance problem is it the state that you get involved these are private homes yeah it's a fascinating question Stephanie who Bears the risk of a homeowner's home ownership if you will and as Alex just mentioned the homeowners are home insurance industry in the State of Florida is really collapsing and without Federal intervention to Bear much of the loss of this storm we would further see the collapse of the homeowners insurance industry in Florida so what do you do who bears that risk the reality is in flood zones there is no private sector product to absorb the risk of a homeowner so the federal government has a national flood insurance program which in your earlier statement only 13 15 percent of of those in this in the strike zone had that that's because only 13 to 15 percent of mortgage companies required it for those those areas so do we subsidize the risk of them rebuilding that is the public policy question right should people actually be able to build in areas where we know we have had in the last five years three major hurricanes Michael Irma and now Ian should private home builders be able to build homes in those areas with the government subsidizing that risk that's a real policy question the one thing I would point out though Stephanie is when we ask questions about floods and hurricanes we also have to aggregate the risks of wildfires in the west of of ice in the Midwest of tornadoes and Tornado Alley how do we handle natural disaster risk is that truly going to be a private sector risk product or is the government going to play a role in that Communities hardest hit Alex let's talk about the communities that were hardest hit they were among the fastest growing in the state is that going to change after Ian think about all the people who moved to Florida in the last few years right Florida has seen an incredible population boom especially after the pandemic uh people really just wanted to come be in this state and Punta Gorda one of the places where the eyewall came ashore was one of the fastest growing cities in the country the last couple of years, so we've seen a massive influx which means there was a lot of people who've never experienced a storm maybe didn't realize the problems of going with the cheapest Insurance you could possibly get maybe didn't realize that they were outside a flood zone the importance of maybe just having flood insurance just in case something like this happened so we're expecting to see you know there's a lot of people that are going to be lining up asking for a lot of money from the federal government from their insurance companies from Charities there is going to be so many billions of dollars of damage here but I have no doubt like people will rebuild back here at Florida really has never learned not to build in places that are scary and dangerous and are going to get walloped year after year after year with storms we see it everywhere you mentioned Irma all those neighborhoods are full backup Mexico Beach where hurricane Michael came ashore a couple years ago all the way full again these communities people do not shy away from them after they're hit in fact they come back, and they build taller houses they build more they build more dents we are clustering our risk around the coast despite the risks of climate change and stronger storms well that is also Who doesn't evacuate because real estate development is one of the most lucrative businesses in this country that has the most in one of the most tax-friendly businesses that get hooked up by our tax code year after year David quickly before we go Florida also has one of the highest percentages of senior citizens people living with disabilities did Florida do a good enough job helping these vulnerable people in vulnerable communities evacuate they can't just hop in their cars and drive yeah listen Florida is very prepared for storms and I think the risk of life would be much greater if we did not have such an experienced infrastructure in the State of Florida uh for storms but I your question is a very good one because I got the question in the last 24 hours who doesn't leave who doesn't evacuate, and the reality is there are a lot of reasons but the most important one is those without means those without opportunity those without the communication that sometimes we take for granted municipalities make public shelters available but how do we make sure that people can get there the the economic disparity is a pressing question in moments like this and I think it's one that should be investigated coming out of Hurricane Ian leaving is a privilege we need to remember that mother nature hits the poorest communities the hardest Alex Harris thank you so much for your work really important reporting down there David Jolly I'm glad you and your family are safe [Music]

Video: Louisiana's Insurance Crisis: Homeowners' policy rates by ZIP Code (7:22)

The state senate is scheduled to talk about bringing homeowners insurance companies back to the state. This comes after a number of companies have either folded or left the state. The house passed two bills yesterday funding the ensure Louisiana incentive program. This program is designed to learn more insurers to the state, giving you more options and hopefully lower cost. The Senate finance committee approved the bills today. Last year many homeowners are dropped by their insurance companies or their premiums went through the group now as the legislature works on lowering homeowners insurance costs eyewitness investigator David Hammer got some exclusive data and found some very big differences and the insurance rates that homeowners pay depending on where they live yeah look for the QR code on your screen during David's story you can scan a photo of it with your mobile device that will pull up an interactive map where you can check out the rates in your zip code and compare them here's our David Hammer investigation not for sale we did a walk-in closet, and then we did darwinda cook was so proud when she finally became a homeowner in her mid-50s this was my dream she brought this house in New Orleans East when it was still damaged and rotting from Hurricane Katrina and turned it into this cozy loving home and that's your bedroom in this movie room but now three years into her dream her homeowners insurance company Americas has folded Cajun Underwriters took over the policy and Cook's insurance agent told her the premium would go from twenty-one hundred dollars to 6700 for the same level of coverage I can't even put into words how how devastating it was the agent found cook of 5300 premium by slashing her contents coverage, but that still takes her monthly mortgage payment from eight hundred dollars to more than fourteen hundred dollars now fourteen hundred dollar house no debt it's not looking good for me Louisiana had back to back devastating storm seasons in 2020 and 2021 to protect themselves from multiple disasters like that insurance companies actually buy insurance themselves it's called reinsurance and it's sold by big companies some with familiar names like Lloyd's of London, but now the cost of that reinsurance has skyrocketed some smaller insurers didn't buy enough reinsurance and went Belly Up others left the state a hundred thousand Louisiana homeowners couldn't get insurance from a private company last year they were forced to go instead to the state-run insurer of Last Resort Louisiana citizens seated premiums written 124 citizens asked Louisiana insurance commissioner Jim Donovan to approve an average rate increase Statewide of 63 percent, and he did because the rates are set by law at 10 percent higher than the highest private insurance rate in each parish and so it varies widely all across the state of Louisiana, and now we've uncovered evidence that the crisis is hitting homeowners in poorer areas even harder we got the premiums Louisiana citizens charged on 19 000 individual homeowner policies last year through a public records request we looked at only about half the policies the ones with two percent hurricane deductibles and twenty-five hundred dollar all perils deductibles and calculated the average premium paid in each zip code for every thousand dollars of insurance coverage purchased, and we found major variations across zip codes for example the average citizens policyholder in darwinda cook zip code 70127 paid 80 percent more for every thousand dollars of dwelling coverage in 2022 than someone in the Lakeview zip code 70124 where property values are significantly higher that makes no sense to cook, and I'm asking like what do you think do you know my address do you know what the darker Reds on the map are the zip codes paying 24 or more in premiums for every thousand dollars in dwelling coverage that's areas near the coast in wafush and Terrebonne parishes Eastern plaquemines parish and Shell Beach in Saint Bernard Parish but it's also New Orleans East and Kenner and the entire West Bank of Jefferson Parish 24 dollars per thousand of coverage really adds up at that rate of one hundred fifty thousand dollar house costs thirty six hundred dollars a year to insure with citizens and that's just the dwelling garages and other structures cost more now the yellows on the map are zip codes that paid less than 16 dollars per thousand on average last year including Lakeview Broadmoor and much of Uptown in downtown New Orleans and remember those are citizens rates for 2022 when citizens raised its rates 63 percent Statewide the average premium in Orleans Parish went up 82 percent meaning that 30 3 600 dollar policy will cost more than sixty five hundred when it renews in 2023. it's where New Orleans East has seen the most increases and that is more because due to open winds coming from two different ways to hit them Cook's insurance agent Stephen wavecchio shows how insurers use models to determine where the risks of storm damage are higher where unblocked winds could hit New Orleans East from the lake and the gulf for instance closer to the river we can get much better rate because the wind modeling is not as bad but Florida State University professor Charles nice says the details of the modeling process are kept secret it is a forward-looking statistical exercise in how frequent are storms how bad are they going to be how much damage and it's it's a simulation that runs thousands and thousands of times Well Vecchio also said insurance companies usually charge more for the first one hundred thousand dollars of dwelling coverage because that amount is usually enough to repair damage from storms fires and other disasters that means someone with a four or five hundred thousand dollar house pays a lower rate to cover most of their homes value than what cook pays for all 1 hundred fifty seven thousand dollars in dwelling coverage she has insurers are not allowed to consider race or income while setting rates but nice analyzed Florida data to see if the methods they use have an unintended discriminatory impact and the answer is yes we do find some statistical evidence it's yet another obstacle for cook by one this grandmother vows to overcome to keep her dream alive this is something that I want that I've always wanted, so I'm I'm not going to just you know let somebody come in and just sweep it away from me David Hammer Eyewitness News again you can check out David's story on wwltv.com and use the interactive map to see the insurance rates in your zip code and compare them with other areas of Louisiana tomorrow night at 10 in part two of not for sale David looks at how State leaders are trying to lower those rates and why some think they're missing the mark.

The National Flood Insurance Policy (NFIP)

The National Flood Insurance Program (NFIP)

If you purchase property in a flood zone, and you have a mortgage, you are required to purchase a flood insurance policy in addition to a homeowner’s policy. The National Flood Insurance Program, (NFIP) was created by legislation in 1968 and has maintained the affordability of insurance for homeowners in flood-prone (both inland and coastal) areas since then. This sounds like a great idea on the surface, but there are some problems with this policy that need to be addressed by Congress.

The NFIP was created to protect property owners in flood-prone areas from disastrous losses in the event of flooding. NFIP, which is managed by the Federal Emergency Management Administration (FEMA) is federally subsidized and kept affordable by borrowing money from the U.S. Treasury in order to keep the program solvent. It is currently in “deep water” so to speak, in fact, it is in debt to the tune of $40 billion. Climate change is complicating the picture. Because of the increase in the frequency of catastrophic flooding in the past 20 years, NFIP has become deeper in debt and in danger of lapsing coverage for property owners. For example, in 2017, many Houston residents whose property flooded in Harvey were not required to have insurance based on their flood zones. This raises further questions about how to manage flood loss in the coming years. The NFIP is no longer a sustainable way to protect property, and it is clear that changes are needed.

Also, although it was not originally intended to do so, the affordability of flood insurance through the NFIP has encouraged development in flood-prone areas, creating an even bigger problem. Homeowners have become accustomed to the availability of affordable flood insurance for their primary residences as well as their second homes on the coast, the number of which has ballooned since the NFIP first came into existence. According to a 2013 study, about one-third of all properties insured under NFIP are second homes (Gaul, 2019).

Without government subsidies insurance rates are likely to increase dramatically, so attempts to change the NFIP have so far been unsuccessful. However, FEMA is in the process of updating the NFIP with the Risk Rating 2.0 Program, which went into effect in 2021.

The overhaul is designed to help address some of the inequity issues with the NFIP and to update the process using current data and technology. New maps are replacing the older FIRM maps and properties are assessed based on their proximity to a water body as well as other features of the property. Raising your property’s height to an additional elevation above the standard base flood elevation* no longer reduces flood insurance premiums, however. You can read about these changes at FEMA: RiskRating 2.0: Equity in Action [5].

The 21st-century rating system, Risk Rating 2.0—Equity in Action, provides actuarially sound rates that are equitable and easy to understand. It transforms a pricing methodology that has not been updated in 50 years by leveraging improved technology and FEMA’s enhanced understanding of flood risk. (fema.gov)

Video: Defining a Property’s Unique Flood Risk (1:15)

[Music] Flooding. It's the most common and most expensive natural disaster in the United States. And, flood risk varies no matter where you live. FEMA has spent decades investing in high-quality mapping data to help inform flood risk and set flood insurance rates. Today we're leveraging that data, along with cutting-edge technology, to get a better understanding of your property's unique flood risk and how that risk can be reflected in the cost of your insurance. FEMA will consider your home's distance to a flooding source, the type and frequency of flooding, and property characteristics, such as the cost to rebuild. With more data going into assessing your flood risk, you'll have a more complete picture of what goes into the cost of your flood insurance. We're making flood insurance fairer and easier to understand to help you protect the life you've built. Learn more about this effort and the benefits of flood insurance by visiting fema.gov forward slash NFIP transformation.

However, there is still work to be done, as in some cases flood insurance has become unaffordable. Lower-income families are having to forego insurance, placing them further at risk. The changes have the potential to change where people choose to build or buy, and the changes are also affecting the livelihood of people who live and work in communities that are flood-prone.

According to the Natural Resource Defense Council (NRDC) in It’s Time to Fix Our Water-Logged National Flood Insurance Program (nrdc.org) [8]:

Congress must act to create a means-tested flood insurance option that helps lower-income families purchase flood insurance, and that prioritizes those same families for flood adaptation assistance. (nrdc.org)

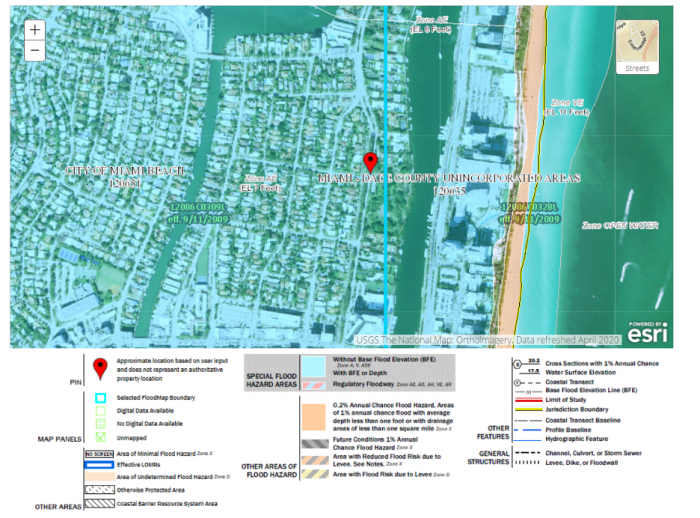

More on Flood Insurance Rate Maps and Base Flood Elevation

Flood Insurance Rate Maps | FEMA Flood Maps Explained [10] are used to determine a property’s flood insurance. A potential homeowner can access these maps before deciding to purchase property in a flood zone. The maps are also designed to help residents of coastal communities plan for and mitigate the flood risk to their properties by delineating flood zones and identifying Base Flood Elevations (BFE). The BFE is the height to which a location has a 1% annual chance of being flooded. A house must be built at or above the BFE to be eligible for flood insurance.

The FIRM zones are based on elevation and proximity to water, as well as several other factors that determine a property’s risk of flooding. Visit this site to read about the flood zones shown on a Flood Insurance Rate Map (FIRM) [11].

Emergency Operation Plans

Emergency Operation Plans

For state and local governments as well as entities such as hospitals, universities, and school districts, developing Emergency Operation Plans (EOPs) is a vital task. An EOP helps everyone who is involved in the disaster management cycle know what he or she should do from the point at which a natural hazard threatens to strike, all the way to the final recovery from the ensuing disaster. It explains who will do what, when, with what resources, and by what authority. Included in these responsibilities is the need to transmit hazard preparedness information and last-minute hazard information to the public. In the response period, when time is in short supply and everyone – from the highest government official to individual householders – is under stress, an EOP helps people respond appropriately and use resources efficiently. See an example of part of an EOP in Box 1.

Box 1: An example of an Emergency Operation Plans (EOP)

Brunswick County is located on the Atlantic coast of North Carolina and is often assaulted by hurricanes. It suffered several direct hits from hurricanes in the 1990s and most recently received a direct strike from category 2 Hurricane Arthur in July 2014. In response to this annual threat, the county in 2008 developed a long and detailed Emergency Operations Plan (EOP) for multiple hazards, including an annex designed specifically for hurricanes.

Presented here are modified excerpts of the hurricane annex to help you understand what an EOP looks like. The first part of this example defines Operating Conditions, or OPCONs, that trigger emergency management actions. There are 5 OPCONs: OPCON 5, Hurricane Season; OPCON 4, Alert; OPCON 3, Stand-by; OPCON 2, Preparation; and OPCON 1, Evacuation. The second part of the example lists important actions to take during the OPCON 2 Preparation phase.

OPERATING CONDITIONS (OPCONs)

The Control and Support Groups will be located in the Brunswick County Emergency Operations Center (EOC) at the Brunswick County Government Center. In the event that it becomes necessary to move the groups to an alternate EOC, the new location will be announced.

OPCON Triggers: To ensure that all activated personnel in the county have a coordinated hurricane response activities approach, the following OPCON levels will be utilized throughout the event.

- OPCON 5: Hurricane Season

This OPCON indicates that hurricane season is open. Brunswick County will stay at OPCON 5 as of June 1st, the start of the hurricane season. At this time, all hurricane plans and procedures should be reviewed. Alert Rosters should be updated and verified. Storms will be monitored and tracked at this level. - OPCON 4: Alert

If the Brunswick County Emergency Management Director determines that a storm could possibly threaten Brunswick County, the County will be moved to OPCON 4. The primary events that will take place at this level are the notification of key personnel of the threat, and initiation of preparatory activities. The EOC (Emergency Operation Center) will not be activated at this stage. - OPCON 3: Stand-By

Once the Brunswick County Emergency Management Director has sufficient information that a storm poses a significant threat, the County will move to OPCON 3. This decision will be based on each of the storm’s specific characteristics. The EOC will be activated at this level, either at a partial or full status. The primary events that will occur include discussing evacuation and conducting pre-evacuation conferences and other preparatory activities. - OPCON 2: Preparation

Once a decision is made to recommend a Voluntary Evacuation or Mandatory Evacuation, the OPCON level will automatically move to OPCON 2. The EOC will be under Full Activation at this level. At this level, shelters will be prepared for opening. Public notification will be coordinated and press conferences coordinated. It is understood that once the County moves to OPCON 2, the County is prepared to commit substantial amounts of money and resources to the effort. - OPCON 1: Evacuation

Once a Voluntary Evacuation or Mandatory Evacuation order is announced to the public, the OPCON automatically moves to OPCON 1. At this level, the primary activity will be the evacuation of the vulnerable population. The EOC will remain at full activation throughout the evacuation and landfall.

EMERGENCY SERVICES

- Manage the EOC Operations in accordance with the Brunswick County EOP.

- Notify the following agencies of the current situation:

a. EOC Operations Personnel

b. North Carolina Emergency Management EOC

c. National Weather Service, Wilmington

d. County Administration / Elected Officials

e. Municipalities

f. Utilities and other stakeholders

g. Adjoining County Emergency Management Divisions - Monitor the weather situation.

- Be available for media interviews and press conferences.

- Install Variable Message Signs at designated locations.

- Begin monitoring traffic patterns and prepare to adjust traffic signals, as appropriate.

- Prepare to implement the traffic assistance plan.

- Complete the establishment of the Amateur Radio Network.

- Position equipment to support evacuation.

- Take appropriate actions to protect critical Brunswick County facilities.

- Coordinate for the movement and/or protection of Fire/EMS equipment during the storm’s impact.

- Assist with status information concerning Law Enforcement Management.

- Prepare to open shelters.

- Coordinate with the PIO for a press release once the evacuation decision is announced.

- Prepare to open Special Medical Needs Shelters if needed. Coordinate with the PIO for a press release once the evacuation decision is announced.

- Position resources to assist with the management of the evacuation traffic. Resources must be in place prior to the start of the voluntary relocation.

- Prepare to conduct “evacuation warning” in the evacuation zones, within the unincorporated portions of the county.

- Implement the security plan in the evacuated areas.

Educating the Public about Tsunami and Storm Surge Preparedness and Warning Systems

Educating the Public about Tsunami and Storm Surge Preparedness and Warning Systems

Educating the public about the existence of warning systems, how they work, and how to react when it is activated are essential components of the preparation.

Tsunami Warning and Public Readiness

In the parts of the United States' most vulnerable to tsunamis – that is, the coastal zones of Hawaii, Alaska, Washington, Oregon, and California – this primarily takes the form of evacuation planning. Anyone driving through low-lying coastal areas of these states is likely to notice tsunami hazard zone and tsunami evacuation route signs lining the roads, and warning signs in beachside hotels and motels.

The National Weather Service’s Tsunami Ready [12]website provides a wealth of guidance for the public about what readiness for a tsunami involves and how to achieve it. Communities can organize tsunami ready training through the NWS program with the goal of achieving community-wide tsunami readiness.

Residents and visitors on the Oregon coast have several location-specific tools to use to learn about tsunami risk in their area and to receive messages about tsunami threats. The State of Oregon Department of Geology and Mineral Resources Oregon Tsunami Clearinghouse [13] is a web site where you can go to get detailed evacuation maps, smartphone apps to aid evacuation, and an interactive evacuation zone map viewer at NVS Tsunami Evacuation Zones [14].

Learning Check Point

Hurricane Storm Surge Warnings and Public Readiness

When a hurricane is approaching the United States and threatens to make landfall, Emergency Operation Plans go into action in the areas likely to be affected. As we mentioned above in the mitigation section, forecasting local storm surge levels can be challenging as it depends on several factors, including the track of the storm, exact landfall location, the timing of the tide cycle, water depth, and the angle and slope of the shoreline, complicating accurate predictions. This, in turn, affects preparation communication.

Therefore, hurricane preparation in a community that may receive a storm surge must start well before the magnitude of the threat is certain for that location. Evacuation orders should be made 72 hours in advance of a storm’s landfall. Many mandatory evacuations have been communicated to the public, only to see the path of the hurricane turn elsewhere. This means that city or county leaders must decide several days out to close schools and businesses, mobilize transportation for those without, prepare shelters, etc. Additionally, all communities within the “cone of uncertainty” of forecast tracks based on modeling, must be on alert and be making preparations. A storm’s track can change significantly during the approach, depending on the steering factors. Hurricane Sally in September 2020 is a good example. Greater New Orleans and Southeastern Louisiana were under a hurricane warning and evacuations and preparation well underway but within 36 hours of landfall, the track moved significantly to the east, so that Mississippi, Alabama, and western Florida received the brunt of the storm surge effects and hurricane warnings were downgraded to tropical storm warnings in New Orleans. Residents of the storm-aware Gulf coast must stay vigilant for these kinds of changes in the forecast.

On a family level, preparedness begins with making a hurricane supply kit (see below) and making a plan for the event of a hurricane. Within 72 hours of landfall, multitudes of decisions must be made, and actions taken. A very abbreviated list of things to be considered in a coastal community threatened by storm surge is: Securing or moving all moveable/ floatable items to a safe place; Securing boats in dock; fueling and moving vehicles, boats, trailers, etc. out of harm’s way; securing the house, by boarding up windows or closing hurricane shutters, and turning off water and power; planning evacuation route and accommodation while away; and communicating with neighbors and family members to ensure everyone has a way to evacuate and a place to go.

Information driving preparedness is broadcast in many ways. A resident in a storm surge zone can best track the storm via local TV news stations and weathercasts to find details about the storm’s impacts in their community. These are often pushed as notifications to mobile devices. The National Hurricane Center [15] provides many kinds of useful graphics that are updated every 4 hours. Mobile Apps are available to access this information too.

{kind=link}

Challenges with Communicating Emergency Plans

Challenges with Communicating Emergency Plans

It is easy to recognize the importance of communicating emergency plans to the public, but many problems can occur in the process. In reality, when emergency information is sent out by a city or state governmental entity, some people will not receive this information, or they may not respond appropriately to it. For example, if the information is broadcast only in English, then non-English speakers in the United States may not fully understand the messages. Poor households in developing countries may not have radios, televisions, smartphones, or other devices needed to receive the information.

Due to many factors (cultural, language, economic, psychological, and social), some people who do receive and understand the government’s communications will choose not to heed warnings and follow instructions given by the government. In the case of Hurricane Katrina, many long-time New Orleans residents chose to stay in New Orleans despite dire evacuation warnings. Among many reasons used for not evacuating, some included: financial constraints on their ability to evacuate the city (typically lack of transportation and no funds for traveling); frequency of hurricane evacuation warnings in recent years (evacuation fatigue); misconceptions about the severity of the storm; perceptions that they were not vulnerable to hurricane risks; worries about leaving pets; and concerns about the need to protect their property from criminal activity.

In many communities in the U.S. and elsewhere in the world, cross-cultural communication has been adopted to ensure all residents receive important messages for preparation for hazardous events. Cross-cultural communication recognizes the diversity of target populations in terms of language and culture, and emergency managers must take these factors into account so that messages are broadcast in the multiple languages spoken in the community in question. Using multiple media platforms and methods for disseminating messages is also essential. The technology available to many people such as texting and social media has helped greatly in recent years. Traditional media like television, radio, newspapers, the Internet, and printed flyers are still important, but other ways of communicating, such as through multiple social media platforms, have become more and more important. Modern communication tends to depend heavily on the mobile or cellular telephone network. In cyclone and tsunami conditions, communication towers can be toppled and rendered useless. In 2005, when cellphone use was common, but texting was less common, loss of communication was an enormous problem across the Gulf Coast following Hurricane Katrina, rendering cellphones useless and greatly hampering search and rescue and preventing people from locating loved ones.

Learning Check Point

Please take a minute to answer the question below. It will not be graded, but it may help you on the Module Summative Assessment.

Creating an Emergency Supply Kit

Creating an Emergency Supply Kit

The Department of Homeland Security’s website: Ready [18] gives guidance to Americans on readiness for all types of emergencies. The section focusing on hurricane preparedness includes this engaging video to catch the viewer’s attention.

Please watch the following short video on hurricane preparedness from Ready - Hurricanes [19].

Video: When the Waves Swell (1:30)

Narrator: When the waves swell, the wind blows, and rain starts to pour you'll ask yourself, how prepared or unprepared are you? Did you board your windows? Protect you home? Secure loose objects so they won't blow away? Bring large items in, and low items up? If you're properly prepared it will help in a big way. Does your family have a plan? Do they know what to do? Is your emergency kit packed waiting by the door for you? Just because you're not on the coast doesn't mean you're okay. Heavy winds and flooding can wash things away. When a hurricane is near, you need to stay safe. Turn on the radio, wait for updates. Only leave your home if told so. Grab your bag and go, go, go. Now if you're home and the heavy wind blows, get away from the windows. Watch out for flooding and protect yourself. You may be without power for a couple days, but your emergency kit should help you to stay. Once the storm is gone and it is safe to go home, be cautious of what's going on. If water is in your path you have to turn back. Dangerous electricity and things you can't see can hurt you very badly. So before the waves swell, the wind blows, and rain starts to pour get prepared. Make a plan, and protect yourself each and every way. America's PrepareAthon. Be smart. Take Part. Prepare. Get started today. Go to ready.gov/prepare

A basic emergency supply kit suggested by ready.gov includes the following recommended items to prepare in case of evacuation:

- Water, one gallon of water per person per day for at least three days, for drinking and sanitation

- Food, at least a three-day supply of non-perishable food

- Battery-powered or hand-crank radio and NOAA Weather Radio with tone alert and extra batteries for both

- Flashlight and extra batteries

- First aid kit

- Whistle to signal for help

- Dust mask to help filter contaminated air and plastic sheeting and duct tape to shelter-in-place

- Moist towelettes, garbage bags, and plastic ties for personal sanitation

- Wrench or pliers to turn off utilities

- Manual can opener

- Paper local maps

- Cell phone with chargers, inverter, or solar charger

I am adding a couple of items to this list from the article in the Tampa Bay Times linked below:

- Camping equipment – Sleeping bags, pillows, and propane stove

- Plenty of cash to tide you over a period of no power for digital payment transactions

- Prescription medications and medical records if health conditions warrant

- Personal documents such as government ID, passport, birth certificate (latter should be stored in a dry box in a safe place if not included in evacuation kit)

Emergency Supply List

Building an emergency supply kit is an important hurricane preparedness activity. Go to Ready [20] and find a document called Emergency Supply List. This is a list that helps you build an emergency supply kit. The document identifies recommended basic items and additional items for adding to the kit. Answer the questions below, identifying the items listed either as a “basic item” or an “additional item” based on this document.

Learning Check Point

Check all that apply for each question

Additional Emergency Preparation Considerations

Additional Emergency Preparation Considerations

Example of Community Hurricane Preparation – Tampa Bay Times

Tampa Bay Times provides readers with very thorough guidance on hurricane preparation:

- Hurricane 2019: The gear you need to stay safe - and comfortable - for the storm [21]

- Hurricane 2020: Protect your home, business, documents, and photos [22]

These two articles cover hurricane preparation – including protecting property and preparing for evacuation. The article covering protecting homes and businesses makes some very important points relevant to any hurricane season, but particularly relevant to 2020, with the extra complication of the COVID-19 pandemic. It emphasizes the importance of planning ahead and making preparations such as purchasing supplies for securing homes and businesses (generators, plywood, storage bins, etc.) early in the hurricane season, and not waiting until a storm threatens.

It also details important tips on storing important documents in waterproof containers ready for evacuation and having a supply of prescription medications on hand for the event of a long period without pharmacy service. The importance of these details may easily be overlooked until the event. Many New Orleanians can attest to this, having neglected to prepare ahead of time and protect essential documents like birth certificates and medical records, which had to be replaced after Katrina. Another really important tip is to have cash on hand. Without power, normal methods of card payment and bank ATM machines and the like do not work. Without cell phone service and power, the ability to access information and to do online banking and shopping is severely curtailed.

In addition, the importance of preparing digital copies of important documents cannot be overemphasized. But this also brings up the importance of taking care of computers and other digital devices and office equipment. File backup onto portable hard drives is essential and once this is completed, if a storm is threatening your area, desktop computers, larger devices, and machines should be powered down and unplugged. All valuables should be moved to the highest points of homes, such as upstairs, if possible. Tablets, phones, etc. should also be backed up but they should be included in the to-go list. It’s important to remember that although you hope you will be able to return in a couple of days after evacuation, this may not be possible. So, preparing for at least one week is important. After Hurricane Katrina, most New Orleans residents could not return for 6 weeks or longer and returned only to survey destroyed properties.

Learning Check Point

This activity will not be graded, but the Module Summative Assessment requires you to have the skills and knowledge it applies. Please take a few minutes to think about what you just learned and answer the questions below.

Summary: Preparedness

Summary: Preparedness

In short, policies that encourage emergency planning, including effective communication of warnings and evacuations, are foundational to protecting people and places from the ravages of tsunamis and hurricane storm surge.