Stakeholders

Stakeholder: A person with an interest or concern in something, especially a busines.

So this is the rest of the “who” after we define the client.

According to the Project Management Institute, project stakeholders are defined as: “Individuals and organizations who are actively involved in the project, or whose interests may be positively or negatively affected as a result of project execution or successful project completion.” An addition to this definition would also include those who believe their interest may be affected by the project. This is a very useful definition as it allows us to cast a very wide net to make sure that all the people and institutions that will be affected by our project are considered.

Stakeholder Identification Process:

While the stakeholder identification process is begun and hopefully very close to completed at the beginning of project development, it is an on-going process with certain stakeholders leaving and potentially appearing as the project evolves. It is therefore very important to be flexible and alert for the disappearance and emergence of stakeholder as the project develops. The specific steps we can take in the Identification Process are:

- Review the project documents

- Brainstorm with your project team

- Communicate

- Develop and maintain a stakeholder register

Let’s take a look at each of the steps to define what we must do to complete these steps:

- Review the Project Documents – There will be certain project documents that can be reviewed to help identify stakeholders. In particular, the project charter and previous Stakeholder registers will be of particular assistance. Your project charter will have identified technology, locale, and size of the project. This should help you think about who the stakeholders will be. Previous Stakeholder Registers will allow the project manager to avoid “re-inventing the wheel.” Other documents which will be important are the various government regulations governing solar development, utility and ISO tariffs, labor standards, impact assessment studies from non -governmental organizations and solar industry standards.

- Brainstorm with your project team - The project team in this case will be your cohort in this course, but if you were working for a solar development company, there would be a project team which would provide you with assistance here.

- Communicate – As stakeholders are identified and brought into the project appropriately, they may also help to identify others who will be affected or need to be consulted.

- Develop and Maintain a Stakeholder Register - This document will allow for documentation of the Stakeholder Management process. Typical information about the stakeholders which will be included in the Stakeholder Register are:

- Name

- Contact information

- Title

- Role on Project

- Interests

- Expectations

- Influence

- Impact

- Internal/External

A full development of the stakeholder register along with the actual information for your locale, technology and client for your project will be required as a completion requirement for the final Project write-up.

Let us now take a look at who the most likely stakeholders for a solar project might be:

- The Client

- The Developer (you)

- The Lender(s)

- The local authorities (we'll get further into this in the policy section

- The State

- The Federal Government

- Labor

- Local non-governmental groups

- State and national non-governmental groups

- Local Politicians

- Local Businesses

- Elements in the non-labor supply chain

See if you can increase the list. Remember to appropriately de-risk the project, the identification of, and communication with, the important stakeholders is paramount from the very beginning.

Certain Stakeholder Roles May Include:

The Developer (you)

The developer is responsible to devise and manage the whole process from ideation to delivery of the project and in many cases through portions of the active life of the project.

The Lender

The lender provides capital dollars to the project. The lender will require statements of satisfactory financial viability ( a Pro Forma among other documents) as well as proof of other approvals (environmental, utility, zoning…)

Authorities at Various Levels

Each of these may have to weigh in or grant certain approvals.

Labor

There are some different facets to the labor question. Making sure that there is appropriate human resources to complete the specific project is important, but there may also be certain areas of backlash as other workers could be displaced by solar energy. There is a significant push to ensure that re-training of energy workers occurs to ensure a renewable energy workforce that is fit for purpose.

Local Non-governmental Groups

There may be local interest groups who are very strong supporters of sustainable development for instance; there may also be local interest groups opposed to your development for reasons such as clashing with the natural landscape.

State and National Non-Governmental Groups, Local Politicians, and Local Businesses

Similar to the local groups support and opposition can be found for solar development which could impact your project.

Elements in the Non-Labor Supply Chain

Supply chain issues are much more prevalent with the current level of solar penetration than they have ever been. Special care to treat these very important stakeholders well will mitigate significant risks in delivery of the project.

See if you can develop these roles further in your own thinking as well as identify more as we work through the course. Please take a look at the sample stakeholder register that has been submitted by a student in AE 878 that is a great example of how to think about this:

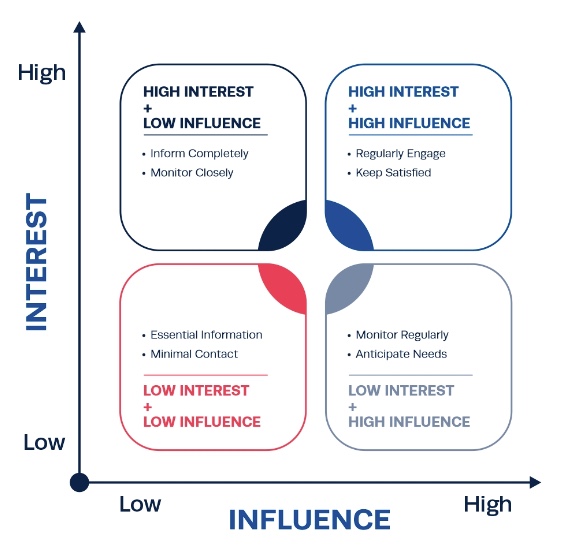

A good way to think about stakeholder management in particular is to look at the following image:

| Low Influence | High Influence | |

|---|---|---|

| High Interest | Inform completely Monitor closely |

Regularly engage Keep satisfied |

| Low Interest | Essential information Minimal contact |

Monitor regularly Anticipate needs |

Here we see the intersection of interest and influence. As we work through the course, see if you can think of the stakeholders that will be introduced and how you might manage them. While this is not a course in project management, we are learning about energy markets through the lens of developing a project.